3 reasons why eurozone inflation is set to fall in 2022

Eurozone inflation will increase substantially over the coming months. However, as this will be mainly driven by one-off factors, 2022 will likely see inflation rates fall again to levels well below 2%

2021 will be the year of increased inflation. We expect a big inflation reshuffle on the back of energy price base effects, social distancing inflation returning, German VAT changes and statistical issues such as changing weights of goods and services in the inflation basket. This could lead some to believe that inflation has made a structural return in the eurozone, but we believe it’s too early to call the return of inflation and we reckon it will drop back far below 2% next year.

The impact on the labour market is deflationary so far

Inflationary one-off drivers have two implications: one is that their impact on year-on-year inflation will disappear the year after. The other is that the impact on the price level will last. This is why one-off inflationary drivers are normally deflationary not inflationary. In the eurozone, the one-off factors driving inflation this year are likely to disappear next year once again. Maybe with the exemption of some longer-lasting reopening inflation. This means that the inflation outlook for 2022 and beyond will be shaped by structural not so much by cyclical factors.

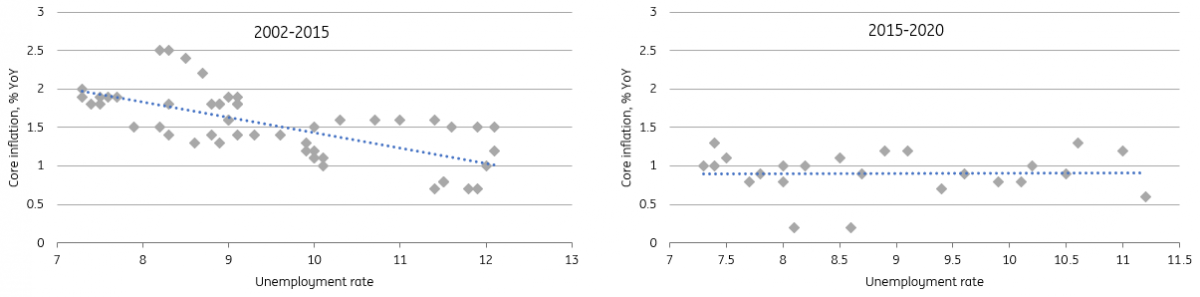

The unemployment and inflation relationship has been declared dead more often than Keith Richards

Consequently, for the inflation path over the medium-term, labour market developments are key. The Phillips curve, which is the relationship between unemployment and inflation, gets a lot of attention although that relationship has been declared dead more often than the Rolling Stones' Keith Richards over the decades. The most recent take on this is that the curve has flattened, meaning that declines in unemployment lead to smaller increases in the inflation rate. With unemployment higher than before the pandemic, labour market price pressures should have weakened, not increased.

The Phillips curve has flattened over time

Even though the labour market shock has been largely absorbed by short-time work schemes in the eurozone, unemployment has gone up. The rate now stands at 8.1%, up from 7.3% in February last year. While it has been coming down from a peak in July, we do expect that unemployment is set for another – perhaps shallow - increase once short-time work schemes end and bankruptcies start going up.

Sure, this is better than the usual impact of eurozone recessions on the labour market, but still results in an elevated unemployment rate. As is common in the aftermath of eurozone recessions, we don’t expect employment to increase materially until labour productivity has recovered, which seems to be a while away still. That means that expectations of a rapid decline in unemployment seem very optimistic for now. We have written more about this here.

A traditional price-wage spiral needs wage inflation

That also translates into wage growth, which has moderated over the course of the pandemic from already slow growth despite being very late in the cycle. While there has been talk of increasing the minimum wage in many countries, these developments have not yet resulted in action so far and even if it would, literature suggests that the impact on inflation would be relatively limited. To put it the other way around: a traditional price-wage spiral needs wage inflation. Right now, it would need political will and decisions to see such a spiral unfolding. Pure market mechanisms in the economy are unlikely to deliver it.

Fiscal support will not be enough to close output gaps, making overheating unlikely

In the US, concerns about overheating occur despite the significant slack still found in the labour market and the large output gap reported. The concerns about the possible persistence of higher inflation relate to the large fiscal stimulus that's just been signed off which could turn the negative output gap rapidly into overheating. How different is the European situation at the moment? The sizable and efficient fiscal support announced over the course of 2020 has had a positive effect on stabilising output, but not much has been announced so far for the recovery phase.

While governments are allowed to overrun the 3% deficit rule under the general escape clause at least for 2021, fiscal accommodation is already becoming weaker in all eurozone countries except for Spain and Greece according to European Commission estimates. Some countries stand to gain sizable amounts from the resilience and recovery fund, but among larger countries, this is limited to Italy and Spain and the spreading out of the disbursements means that not too much is to be expected of it in the short-run.

Fiscal support is waning as eurozone governments are set to reduce budget deficits

Look to history

This means that output gaps are likely to remain sizeable over the course of 2021 and 2022, which makes it hard to see how structurally higher inflation would occur. According to European Commission estimates, the output gap is likely to remain above 2% for Italy, Spain and France in 2022, with the Netherlands and Germany performing slightly better. Historically, this corresponds to a recessionary environment still which means that inflationary pressures will remain weak.

Negative output gaps generally come with a weak inflation environment

But... imported inflation could trend higher on a more structural basis

Not all factors point to a lacklustre inflation aftermath of the coronavirus crisis. The global economy is leading the eurozone in terms of economic recovery, which itself is leading to bottlenecks in the economy that already increase pipeline inflation substantially. China has already recovered to pre-pandemic levels of GDP, while the US is set to reach that level over the course of the summer. With concerns about overheating in some large global markets, there are even talks of a commodity supercycle, with potential knock-on effects on eurozone prices.

Non-energy commodity prices have reached their highest level in just under a decade

There is a chance that this will last past the initial reopening phase given factors like the large stimulus program in place in the US. Our expectations of a relatively strong euro do counteract this issue to a certain degree though. It has to be said that the passthrough of a stronger exchange rate on inflation has weakened over time, but overall it does provide some comfort for our call that import prices will be dampened a bit in times of potential global overheating.

Expect inflation to fall back, but be slightly higher than pre-pandemic levels

In times of huge uncertainty like the one we’re currently in, an economic outcome with structurally higher inflation is not unimaginable. Still, almost all domestic factors point to a return to lacklustre inflation once temporary effects run out of the data. Global economic factors could have a longer upward impact on inflation and so could second-round effects but in our view, it is unlikely that this will keep inflation above 2% in 2022. If you look through all of the noise, the pandemic is ultimately deflationary and that will at some point show in the numbers.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more