US: Happy shoppers

Decent US retail sales numbers suggest consumers are shrugging off the negative trade headlines and support our view that markets may be too aggressive in their interest rate cut expectations

A healthy number, with significant upward revisions

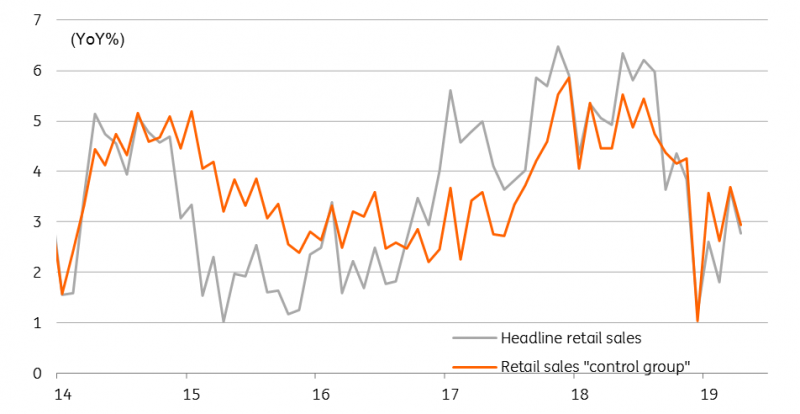

US retail sales for May are broadly in line with expectations, but significant upward revisions give the report a positive glow. Headline sales rose 0.5%month on month versus the 0.6% consensus prediction, but April’s figure went from -0.2%%MoM to now become +0.3%. The “control group” which strips out some of the volatile components, such as autos, gasoline stations and building materials, was actually a touch above expectations, rising 0.5%MoM versus the 0.4% consensus, while April’s figure is now +0.4%MoM growth versus the 0% figure originally reported.

Employment continues to grow and wages are rising, so households have money to spend

We already knew that auto unit sales surged 5.5% in May, but this has only been translated into a 0.7% increase in the value of auto sales, thereby suggesting some fairly steep price discounting last month. Gasoline station sales were little changed since in seasonally adjusted terns prices fell modestly. Outside these components, the story was pretty solid with sporting goods and electronics both up 1.1%, general merchandise up 0.7%, non-store retailers seeing sales rise 1.4% and health up 0.6%. Food was a little weak, falling 0.1% while clothing, furniture and building materials were little changed.

US retail sales heading higher

Spending looks resilient

In general, there has been some softening in the recent economic data, but we remain upbeat of the prospects for retail sales and consumer demand more broadly. Employment continues to grow and wages are rising, so households have money to spend. Asset prices remain robust as well so this is all helping to support consumer sentiment.

The fact that consumer confidence has only been higher on four occasions in the past 18 years suggests that spending should be pretty resilient even if we get some further negative news on US-China-Europe trade relations. So while the Federal Reserve does seem to be shifting towards rate cuts, market expectations of 100bp of easing look too aggressive to us.

We look for 50bp of easing in 2H19.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more