3 calls for the US economy as it heads toward recession

The Federal Reserve has made it clear it is prepared to sacrifice growth in order to get a grip on inflation via higher interest rates. We see the clear risks of retrenchment in consumer spending, fuelling recession fears

Recession is technically possible, but it will feel more real at year-end

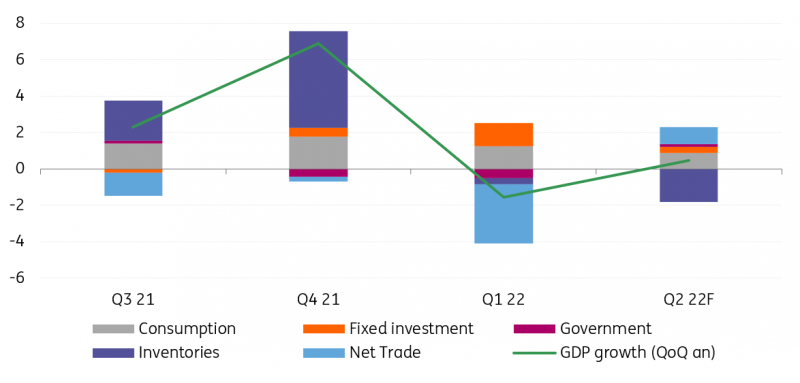

The US economy contracted 1.6% in the first quarter of 2022 due primarily to a massive trade deficit as strong domestic demand sucked in imports, but Covid constraints and port disruption elsewhere limited export growth. Unfortunately, the latest revisions also show consumer spending was not as strong as we were initially led to believe, while monthly data suggests that momentum weakened further in the second quarter as confidence faltered due to the rising cost of living and the threat of higher interest rates. With inventories being run down once again, we can’t rule out the possibility that our tepid 0.4% quarter-on-quarter annualised second-quarter growth forecast ends up becoming a second consecutive negative GDP print. This would meet the technical definition of recession.

Contributions to US GDP growth

3Q 2021-1Q 2022 with ING's 2Q 2022 forecast

However, we doubt that the National Bureau of Economic Research’s Business Cycle Dating Committee would list this as an official recession given the economy is still experiencing rising consumer and business spending and falling unemployment. However, we suspect this will only be a temporary reprieve with a strong chance of broad-based economic weakness in late 2022/early 2023.

With confidence already looking weak and the housing market showing clear signs of faltering as a lack of affordability and rising mortgage rates weaken demand, we are nervous that consumers will soon stop relying on accumulated savings to maintain their lifestyles through the current cost of living crisis. Moreover, the Federal Reserve has made it clear it is prepared to sacrifice growth as it desperately tries to get a grip on inflation via higher interest rates. This is also contributing to the strongest dollar in 20 years, which will hurt international competitiveness. In this environment, we see the clear risks of retrenchment in consumer spending while falling corporate profitability means businesses start to hunker down.

Inflation to fall back to 2% by end-2023

Inflation is at 40-year highs and is likely to remain at extremely elevated levels for the next six months due to high energy costs, rising food prices, and an ongoing strong contribution from housing costs tied to rising rents and home prices.

However, we are increasingly convinced that inflation will fall sharply through 2023. If the housing market slows rapidly this can translate into a sharpy reduced contribution from shelter within CPI (35% of the basket). Second-hand cars have also been a major factor contributing to elevated inflation this year, having risen more than 50% since February 2020, but if the availability of new cars improves this could lead to a collapse in prices for second-hand vehicles. Given its chunky weighting within CPI of more than 4%, this too can help get overall inflation sharply lower.

Higher interest rates will also take more of the steam out of the economy and weaken corporate pricing power, potentially even leading to some profit margin compression. Then, if we can get some relief from the supply side of the economy, and if energy prices top out and potentially even fall in 2023, this can build a strong case for 2% inflation before the end of 2023.

Rate cuts to be on the Fed’s agenda for summer 2023

We look for the Federal Reserve to follow up June’s 75bp rate hike with another 75bp move in July before switching to 50bp moves in September and November with a final 25bp hike pencilled in for December. This would leave the Fed funds rate range at 3.5-3.75%, which we think will mark the peak given our growth and inflation forecasts.

With the Fed having acknowledged the risk of recession from its moves to get a grip on inflation, it will require the central bank to be convinced that inflation is heading back towards 2% before it will seriously contemplate loosening policy.

ING's Fed funds rate forecasts (ceiling of range %)

However, as already suggested, we think that inflation has the potential to fall very sharply from 2Q23 onwards. This could open the door to rate cuts as early as summer 2023 with history showing that over the last 50 years the Fed has cut rates on average just six months after the last rate hike in a cycle. We expect the last rate hike to be in December this year and that would suggest a June 2023 timeline for the Fed moving from a “restrictive” monetary policy toward a more “neutral" one.

Download

Download article

7 July 2022

ING Monthly: Europe’s recovery is cancelled This bundle contains {bundle_entries}{/bundle_entries} articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more