Sterling unprepared as UK-EU trade deal hopes fade

The chances of a UK-EU trade deal being struck are now 50:50 at best, given the events of the past few days. The very limited risk premium factored into EUR/GBP at the moment suggests further downside lies ahead for the pound

The chances of a deal have receded

The UK government’s unveiling of its Internal Markets Bill marks the start of what promises to be another messy period in the Brexit saga. Provisions contained within the bill to effectively disregard parts of the withdrawal agreement have undoubtedly reduced the chances of a deal, and we think at best the odds of a free-trade agreement being reached this year are now 50:50. For sterling, this is likely to mean further downside ahead. No trade deal could see EUR/GBP trade above this year's high of 0.95.

What follows is an explainer of what's been happening, and what it means for the chances of a deal and the pound.

State aid is the UK government's main concern

State aid is the dividing issue in Brexit talks, and the UK government is keen to retain a free hand to support British industry once the transition period has ended. The EU, in contrast, wants adequate reassurance - if not in the form of ECJ oversight, then perhaps via an independent regulator - that the UK won’t abuse state aid in a way that could put European firms at a competitive disadvantage.

But the UK’s ability to engage in state aid is also bound to a certain extent by the terms of last year’s withdrawal agreement. The government is obliged to follow EU rules on state aid rules where intervention might affect trade between Northern Ireland and the EU.

One concern in Westminster is that this could seriously restrict its ability to support companies in so-called industries of the future.

What does the Internal Market Bill do?

This appears to be a key motivation behind the legislation published by the UK government on Wednesday, which effectively seeks to give ministers powers to disapply the state aid provisions contained within the Northern Ireland Protocol - the formal name for what was once termed the Irish backstop.

It also looks to override the terms of this agreement on the need for customs declarations and tariff payments on goods crossing the Irish Sea.

Does this kill the chances of a deal?

Despite some talk that the government might water down the powers granted by the bill, the published legislation is perceived to be just as incendiary as was reported in the FT over the past few days. And ministers have made no secret of the fact that these moves could leave the UK in breach of international law.

This raises a few questions.

Firstly, what will the EU make of all of this? So far, the response has been relatively cautious. Brussels hasn't formally said it will suspend talks. And according to the Irish Times, the view in Dublin is that the bold nature of this newly-published legislation means it is most likely “sabre-rattling”. The EU has however since called a meeting of the ‘joint committee’, which was set up to fill in the blanks in the Northern Ireland protocol agreed last year.

Secondly, there’s a clear question mark over how the House of Lords will treat this legislation. A number of political commentators have highlighted that the bar is pretty high for it to pass, given concerns about abiding by the law.

Thirdly, there are some faint parallels with what happened this time last year. Parliament was prorogued, a move that was later ruled to be unlawful by the Supreme Court. And while there is still plenty of discussion about exactly what the goal of all of that was, it may well have been partially designed to inject some pressure, or a sense of crisis, into negotiations. Whether or not this tactic contributed to the agreement of a revised deal last October is of course debatable.

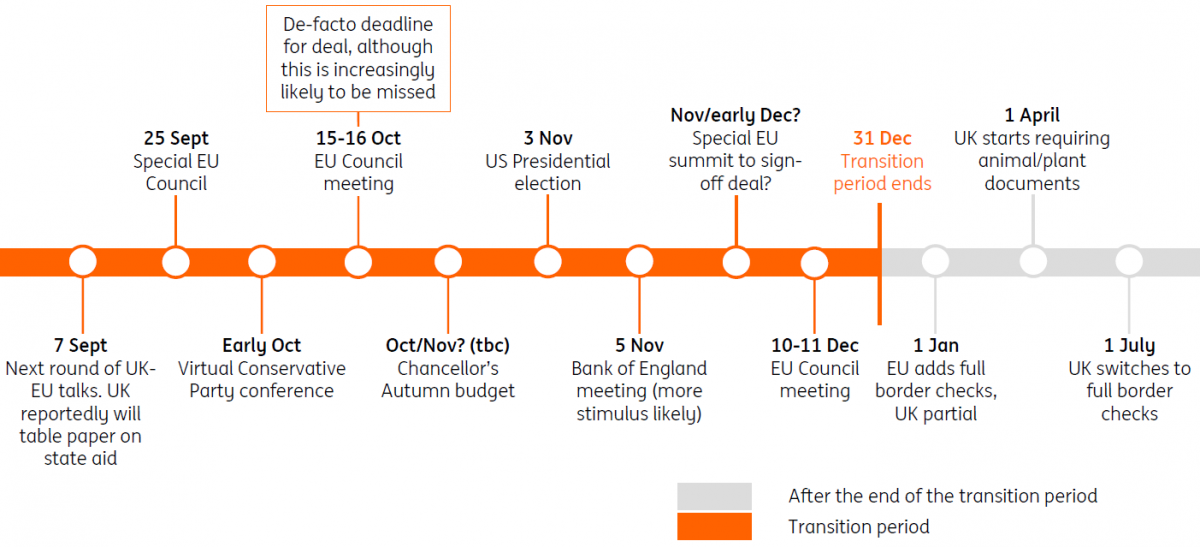

The latest Brexit timeline

Don't write off the chances of a deal

The upshot is that despite all of this latest drama, we probably shouldn’t completely write off the possibility of a deal being done at the eleventh hour, although there’s little doubt the probability has diminished.

The Internal Market Bill is likely to diminish trust even further between negotiators, and the EU will be very wary of signing a free-trade agreement while there’s a risk that the UK could go back on its earlier commitments.

Equally, while some of the above may indicate that the government isn’t completely against a deal, at least not as much as the recent fireworks would seem to imply, PM Johnson has also publicly indicated that he doesn’t believe ’no deal’ would be a disaster.

And that leads us to a potential counterpoint to the 2019 vs 2020 argument above. The ‘compromise' PM Johnson reached with the EU last October in effect moved the needle towards a more arms-length future relationship, the kind of agreement he was arguably more comfortable with. The change from PM May’s deal meant that the UK would no longer remain permanently in a customs union with the EU.

This year, it’s a different story. A compromise would involve ceding some control on state aid, if not directly to the EU, but to an independent regulator, and as we know, the UK government is highly reticent to do so.

So where does all of that leave us in terms of probabilities?

In honesty, we think it’s pretty much 50:50 now, and perhaps the bias is if anything towards ‘no trade deal’ at this stage.

But either way, we think the de-facto mid-October deadline will be most likely be missed. The jury’s out on how much longer talks can run, be it in public or behind closed doors (the so-called ’tunnel’), while still allowing some time to ratify a deal if there’s going to be one. There’s a growing sense though that the saga could easily stretch into November

With-or-without a trade deal in place, the end of the transition period will herald a raft of new costs for businesses, and that's likely to drag on the post-Covid recovery. Read our economic analysis in our latest monthly economic update

GBP: Limited risk premium means potential for further downside

We continue to see GBP as unprepared for the stream of downside risks ahead discussed above, and following the market complacency during the summer months, we estimate that only a limited degree of risk premium, as you can see below, is priced into the currency (just around 1% in EUR/GBP vs 5% risk premium pricing in late June). This allows for a further GBP decline.

We look for EUR/GBP to break the multi-month high of 0.9176 in coming days. Not only is a limited degree of risk premium is priced into GBP, but the speculative positioning does not seem stretched (the latest CFTC data still show a neutral positioning in GBP/USD), in turn allowing for a build-up in GBP shorts which would help facilitate further GBP downside.

As we noted in this article, GBP: Summer is over, brace for the reality check, should there be no trade deal, we expect EUR/GBP to break above this year’s high of 0.95 and potentially test parity.

Indeed, even with a limited deal in place, the change in UK-EU trade terms would leave the UK at risk of a slower recovery versus its peers, taming the potential medium-term upside to both GBP spot and its fair value. In the case of no trade deal being agreed, such a trend would gain even more traction and, coupled with the likely response and more easing from the Bank of England, which could include the possibility of negative interest rates, the outlook for sterling would clearly deteriorate and the currency would come under further pressure.

EUR/GBP risk premium

Download

Download article11 September 2020

Brexit, the pound, and the ECB’s possibly risky verbal balancing act This bundle contains {bundle_entries}{/bundle_entries} articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more