Safe haven buying boosts gold prices

Concerns over the banking sector have led to a move towards safe haven assets and gold has clearly benefited from this. While we see a short-term pullback in prices, we expect these to strengthen over 2H23

Speculators boost gold long

Growing concerns in the banking sector have led to a flight to safety and gold has benefited. CFTC data shows that speculators have boosted their net long in COMEX gold in recent weeks. The managed money net long has increased by 67,047 lots since late February, to stand at 106,955 lots. Speculators had already increased positioning towards the back end of last year and the start of this year - on the expectation that the Fed is not too far from the peak fed funds rate.

There is still room for speculators to boost their positioning further. The right catalyst could come in the form of banking sector concerns lingering and signs of inflation easing, these signalling a potential pivot from the Fed.

A number of measures suggest speculators still have room to increase their exposure to gold:

Net spec position - The current net long is slightly below levels seen in January this year, well below levels seen at the start of the Russia/Ukraine war, significantly lower than levels seen over the peak covid lockdown period and below the record net long of around 292k lots seen back in September 2019.

Net spec position as % of open interest - At the moment, the net spec long in COMEX gold makes up around 22% of open interest. In the past we have seen spec length at as much as 50% of open interest. This was the case in 2016 as well as in 2019.

Long/short ratio - Currently the long/short ratio for speculators in COMEX gold is 3.72. This is well below the record of more than 90 seen at the peak of Covid lockdowns, and also below the 2018-22 average of 5.48.

USD value of spec position - It also makes sense to look at the speculative position in USD terms. At the moment the value of the net spec long in COMEX gold is around US$21b. While this is a big increase over 2H22 levels, it is still well below the US$40b plus seen over parts of 2019 and 2020.

Speculators still have room to increase long positioning

Gold ETF demand grows

2022 saw significant ETF outflows for gold, particularly over 2H22. Over the full year, the gold market saw ETF outflows of a little more than 110 tonnes, and the second consecutive year of net selling. Despite the strength in gold prices at the start of this year, we continued to see ETF selling over January and February. World Gold Council data shows net outflows of 61 tonnes over the first two months of the year. Some strong US economic data (US jobs and CPI data) helped to raise doubts over how soon we could see the Fed pivot.

Over the past 2 weeks we have seen this trend reverse, reflecting the risk-off move and the flight to safety. We have seen ETF net buying of 36 tonnes in the two weeks ending 24 March. ETF holdings will largely depend on developments in the banking sector and how successful policy makers are in restoring confidence. Containing worries would likely lead to a short term pullback in gold prices.

Central banks remain keen gold buyers

Weak ETF demand in 2022 was offset by strong central bank buying. Central banks bought almost 1,136 tonnes of gold last year. Turkey and China were the largest known buyers, adding 148 tonnes and 62 tonnes respectively. This strong buying has continued into 2023, with Turkey and China adding a further 23 tonnes and 15 tonnes respectively in January 2023. We expect central banks to remain buyers, not only due to geopolitical uncertainties but also due to the economic climate.

Fed policy should support the gold price later in the year

ING’s base case is that we are not on the verge of another financial crisis following recent developments in the banking sector. Issues in Europe were addressed through prompt intervention from the Swiss government. In the US, issues are isolated to non-systemic banks and larger banks have seen an increase in deposit inflows. Recent developments suggest that the Fed does not need to tighten significantly further - it appears that rates are already in restrictive territory.

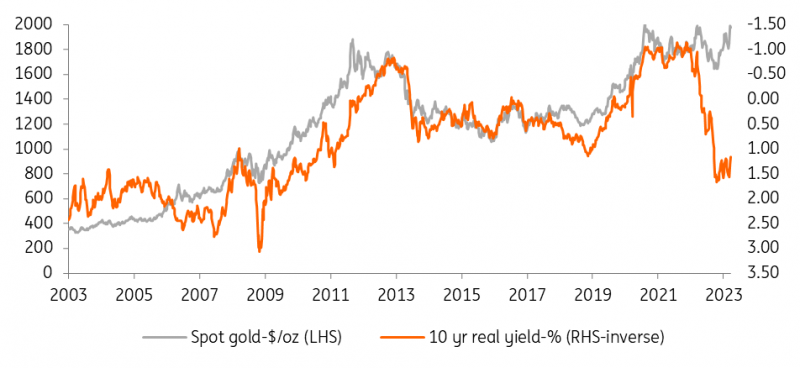

Fed policy is likely to be key for gold over the medium term. The Fed is likely approaching a peak in the Fed funds rate, and we could see a pivot over the second half of this year. Recent events suggest that credit flows will become more restrictive - this will weigh on the economy and allow inflation to fall even faster. Our US economist sees a final 25bp hike in May, which would leave the Fed funds range at 5-5.25%. Rate cuts will likely then become the theme for 2H23, and we see the Fed cutting by 75bp in the fourth quarter. We would expect real yields to follow policy rates lower later in the year, which should prove supportive for gold prices.

Whilst we expect a pullback in prices in the short term, we see gold prices moving higher over 2H23, and expect spot gold to average US$2,000/oz over 4Q23. The assumptions around this are that we do not see further deterioration in the banking sector and that the Fed starts cutting rates towards the end of this year.

Spot gold vs. US 10-year real yield

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more