Rates Spark: Why central banks struggle to control interest rates

The Fed is set to kick off its tightening cycle today. Whether this translates into durably higher long-end interest rates depends on the market’s economic optimism. The energy crisis means there is less of it. After an overshoot, rates should settle near current levels

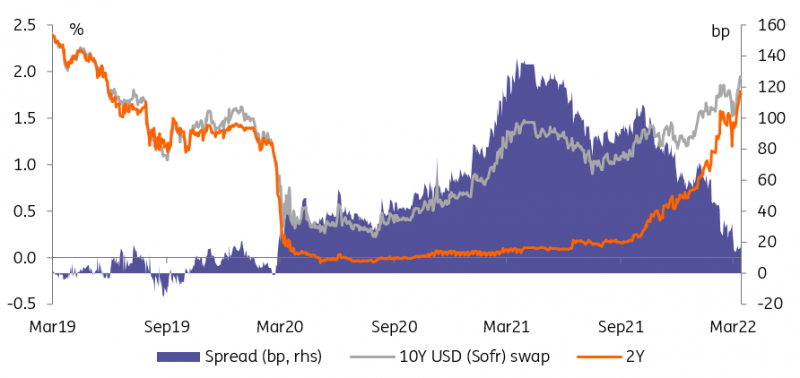

Curves have flattened as hikes got closer

As the Fed is about to embark on the first of what we expect will be an eight times 25bp hiking cycle, it is useful to remind ourselves of the role central banks have in influencing long-dated interest rates. In all likelihood, a more hawkish Fed, for instance moving its dot plot to close to the number of hikes we’re expecting in this cycle, would push rates higher. The fact that the curve is already pricing a path very close to our own expected trajectory for the Fed Fund rates suggest that this would be far from a surprise, however.

A flatter curve signals the market's view about how far a central bank can hike

Balance sheet reduction is likely to be phased in over the second half of this year, an eternity in financial markets

In theory, its tone would also help inform markets about the fate of its balance sheet reduction plans, something that should, in principle, influence long-dated interest rates more directly. In practice, it hasn’t worked out that way. The more hawkish the Fed has got over the past six months, the flatter the curve has become. This probably reflects, in part, the fact that interest rates policy remains the Fed’s primary policy lever. There is also a timing argument. Balance sheet reduction is likely to be phased in over the second half of this year, making its impact three to six months away, an eternity in financial markets.

Higher interest rates need economic optimism

This brings us to our main point. Central banks have a much better track record of influencing short-end interest rates, even in the age of Quantitative Easing (QE). Whether a more hawkish central bank translates into higher long-end rates depends in large part on market optimism that the economy can withstand higher rates. This may be less of a concern in the US than in the Eurozone but the energy crisis has chipped away at confidence in central banks’ ability to raise rates for long, hence the flat or inverted yield curves.

Economic angst means markets now see cuts in 2024 as a possibility

We’re probably closer to the end of the adjustment higher in rates than to its start

In our view, we’re probably closer to the end of the adjustment higher in rates than to its start. In the near term, rates are on an upward trajectory and we think the odds of US Treasuries overshooting our 2.25% forecast are good. The same goes for 10Y German Bund rising above our year-end forecast of 0.60%. In the medium term however, the front-loaded path signalled by central banks and implied by financial markets should also limit long-end rates’ ability to rise much further.

Today’s events and market view

The main economic releases today will come from the US: retail sales and housing market index.

US events will culminate in the March FOMC meeting, statement of economic projections, and Powell’s press conference. Markets will pay special attention to revised interest rates projections, the famed dot plot, and to growth forecast as higher energy prices bite. Absent further upward surprises on inflation in the coming months, we think markets will regard any dissent in favour of a 50bp hike as something that will remain a marginal view.

Another question is whether the Fed decides to hike the interest on excess reserves and the reverse repo rate by the same 25bp as the target Fed Fund range. Over time, we think the latter could be brought back in line with the lower band of the range, pushing more liquidity into other money market alternatives, but there is no need to rush that decision today.

In European hours, there are scant data to move markets but Germany will auction 10Y debt.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more