Rates Spark: The range is your friend

Through the recent gyrations, markets seem to lack the conviction needed to push new lows in rates. The resulting range-trading environment brings lower rates volatility and better risk appetite. We think rates differentials should narrow when rates finally converge lower

Not enough conviction to call time on inflation, and still divergent policies

The China reopening hype seems to have faded, judging by commodity prices running out of steam already. This is at least one less source of inflation for markets to fear but it is fair to say that coordinated central bank tightening, as was the case in 2022, doesn't rank very high on the market's list of worries. Instead we may well be witnessing a market where better-than-expected growth is causing investors to shun long-dated bonds when yields fall too fast. This theory is only valid up to a point. Recent hard German data, for instance industrial production, is showing an economy unlikely to reach escape velocity any time soon. And yet, European bonds have pulled back just as hard as their US counterparts.

Better-than-expected growth is causing investors to shun long-dated bonds when yields fall too fast

The net result is a curve is no hurry to print new lows in yields due to better opportunities in other markets, and with not enough information to push rate cuts expectations lower. Similarly, revisiting the 2022 highs seems out of the question, even accounting for the fact that yield curves, especially in the US, are deeply inverted. Combine this with still divergent policies with the Fed near the end of its hiking cycle, and the European Central Bank unsure where its own cycle will end, and we have a powerful force pulling yields away from the extremes of the recent range.

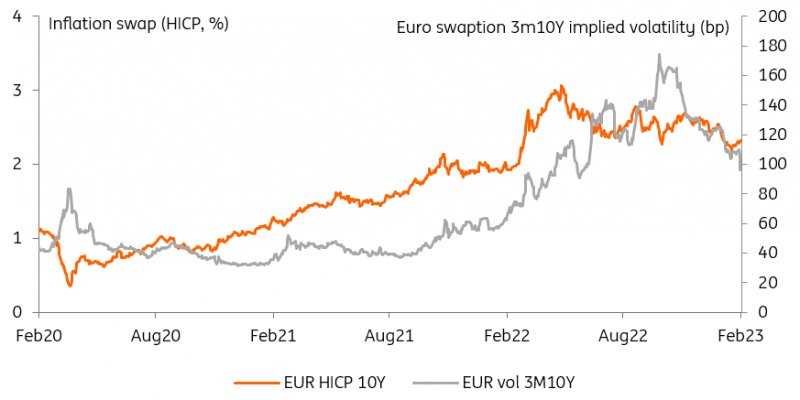

Lower inflation expectations and the resulting decline in volatility are boosting risk appetite

Lower rates volatility is good for risk, and rates differentials should narrow

There are two themes emerging from this state of play. Firstly, rate implied volatility in the option market is right to decline from last year's highs – even taking into account last and this week's gyrations. This is an environment, as we've seen, conducive of greater risk appetite, and also a reason why investors would shun the safety of government bonds, except perhaps for the shorter ones.

This is an environment, as we've seen, conducive of greater risk appetite

The other theme is that this market is less likely to see large directional moves, even though we think the trend in rates is still lower. Instead, the most remarkable moves are likely to be in cross country spreads. Notwithstanding a solid US job market, we continue to think US rates have further to fall than their European counterparts. Last week has shown that this sort of view is not immune to setbacks, but we think it is the one most consistent with rates taking their time to converge lower, and happy to pause for a while, within existing ranges.

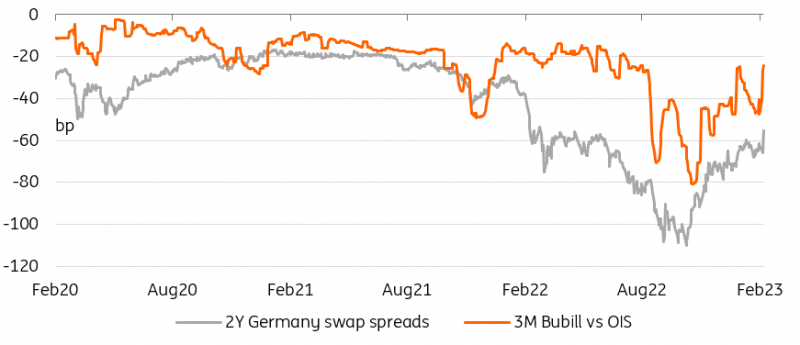

Short-end swap spreads should tighten further on reduced collateral scarcity fears

The ECB has chosen to nip any re-emergence of collateral scarcity fears in the bud

The ECB has announced the post-April remuneration arrangements for government deposits held at the ECB last evening. These deposits will no longer be remunerated at ESTR, but at 20bp below – very generous compared to the prospect of a 0% cap kicking in again. Fears of €350bn in government cash suddenly pushing into the tight collateral market now give way to an outlook of a more gradual adjustment, which will be easier to absorb for the market. The move shows the ECB’s sensitivity to market concerns in this area and removes a major obstacle to the further structural tightening of Bund asset swap spreads.

Today's events and market view

What we lack in data today is compensated by a busy slate of central banks speakers and brisk supply action. From the Fed we will hear from a wide range of officials including Williams, Cook and Kashkari, though it should appear that with Fed Chair Powell's comments yesterday the central bank's main take on the data should be clear – no need to ratchet up the hawkishness on one data print.

Over in Europe ECB’s Isabel Schnabel stated yesterday that the ECB’s unprecedented tightening had little impact so far on inflation, signalling that rates would have to remain in restrictive territory until there is robust evidence that underlying inflation is coming down. Klaas Knot, another outspoken hawk, is scheduled to speak on the economic outlook today. Recall that in January he had called for rate hikes also in May and June.

After Powell failed to dial up the Fed's hawkish message, we expect risk sentiment to continue improving in the short term. As we discussed above, we're increasingly in a market where this means bond markets fall out of favour with investors, and yields drift higher. 10Y Treasuries are within touching distance of 3.75% but this may take a little while longer to get there if volatility dies down as we expect. The hawkish ECB push should help at the margin although we think the message has already been clearly delivered in recent days, despite a few doves' dissent.

In supply the focus will shift to the US longer end with the US$35bn sale of a new 10Y note, followed by the 30Y tomorrow. In EUR goverment bond markets Germany reopens a 7Y bond and Portugal a 10Y. The UK sells a 17y Gilt.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more