Rates Spark: No Covid rally for bonds

Focus turns to syndicated bond deals, with borrowers hoping for no new volatility from this week’s key economic releases. By and large, rates markets seem to have acquired a good deal of Covid immunity. This is in part due to ECB purchases being largely decided for the year already. With the US 10yr back in the 1.7% area; now what? Keep rising until bought into

Here's why US rates have risen strongly from the off in 2022

Elevated inflation is not a new story, but the Fed is an evolving one. An accelerated taper, and a quick step towards rate hikes is on the menu for 1Q and 2Q. That's not a "next year" story any more. It's front-and-centre, which helps to concentrate minds.

As always when we get these moves there is a debate as to whether this is a price or quantity driven event

As always when we get these moves there is a debate as to whether this is a price or quantity driven event. So far I see it as a price driven one. In other words, it is not being driven by huge volumes. It is more driven by a re-calibration of yields towards more sensible levels, without much resistance. Hence big moves have been achieved with relative ease.

It does feel like this can continue. It is reminiscent of the move we had in Feb/Mar 2021. That ground to a halt as the 10yr hit the 1.7% area and was met by a wave of fixed rate receiving and a re-build in duration exposure. This time it feels like we can push beyond that, to more elevated levels before market longs step in.

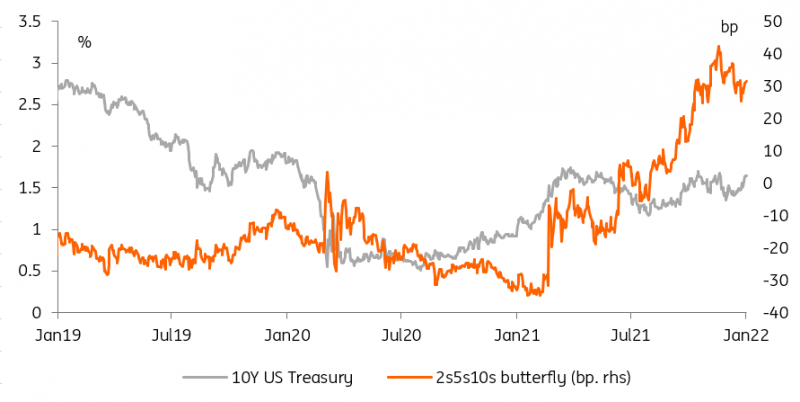

10Y yields are on the rise, and 2s5s10s indicate more is to come

There is a lot of talk of 2%, so we'd guess the approach of within 10-15bp of that is where the longs could well begin to take an interest. But it also depends on how fast the move is. Players will not come in to play this from the long side if there is real aggression to the sell-off. So far that is the case, and it looks like we should grind higher.

The structure of the curve also remains bearish and braced for rate hikes

The structure of the curve also remains bearish and braced for rate hikes, with the 5yr cheap to the curve. It can get even cheaper. The 2yr approaching 80bp is getting set too (as is the 2yr swap at 95bp). But the 10yr, which began the year at 1.5%, was always liable to get pressured higher. The thing that kept the 10yr under wraps in 2H 2021 was net buying / net inflows.

The key for us is whether that net buying / receiver interest kicks in again. It might. But will be more difficult if the Fed is intent on hiking, and hiking fast. A fixed rate receiver may be positive in carry, but that carry gets eaten away every time the Fed hikes.

Hoping for uneventful data ahead of a wall of supply

In a week peppered with economic releases, issuers flocking to primary markets will be hoping for no major deviation from the numbers expected by economists. In Europe, French CPI actually came in slightly below consensus yesterday, so the hope is for a similarly underwhelming outcome from Italy today, from Germany on Thursday, and the Eurozone on Friday. Another spike in prices would make new syndicated deals all the more perilous but, December Eurozone inflation is expected to have declined, led by Germany.

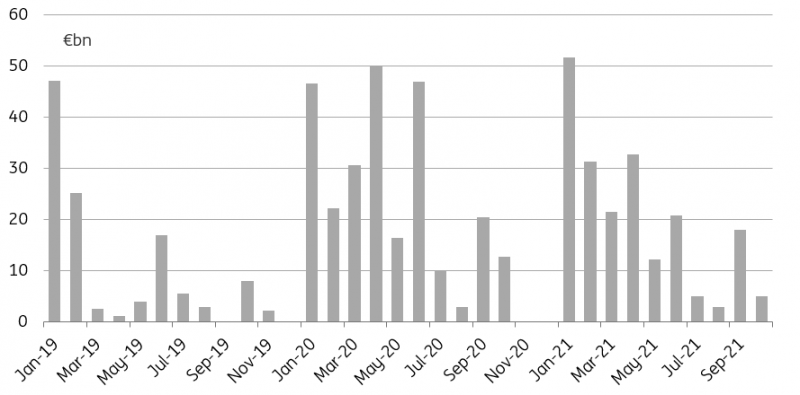

EUR sovereign syndicated supply typically spikes in 1Q

Bond markets can also count on a potential relief rally if Italy, having mandated banks for a 30Y deal yesterday, is the only major Eurozone syndication that materialises this week. In any case, the relief is likely to prove short-lived as next week will bring a flurry of additional deals. Fortunately for borrowers, the profile of ECB purchases in 2022 is likely to follow a pattern not unlike that of bond supply: with the busiest quarter at the start of 2022 and a gradual decline as the year progresses.

Covid-19 no longer brings lower rates

This being said, the balance of supply and demand in 1Q 2022 will still look different from 4Q 2021, with PEPP purchases declining at the same time as bond sales surges in line with previous years’ seasonality. This, and the lack of central bank purchases in the final week of 2021 go some way to explain the rise in EUR rates in recent days. Also, with the amount of ECB purchases all but set for 2022, the bar for further ECB intervention in the bond market appears higher to investors, even in the face of another Covid-19 wave.

The bar for further ECB intervention in the bond market appears higher to investors

On the face of it, there does not seem to be much change in macro conditions that would justify the recent rise in yields. The continued rise in Covid-19 cases bodes ill for hopes of quick economic reopening. Beneath the surface however, markets are finding solace in European governments’ reluctance to inflict new restrictions on their economies. Add to that uncertainty as to how the current wave will impact inflation dynamics, with further supply chain disruption for instance in China, and the risk of longer labour shortages, all keeping bond holders on their toes.

Today’s events and market view

Today’s batch of economic data starts with the final reading of European PMI services. Spanish and Italian indices on the other hand will be first releases. The European morning will also bring a first look at Italian December CPI, after the French equivalent came in slightly lower than consensus yesterday.

Barring a large deviation of economic data from expectations, it is likely that the attention will be stolen by the first of the heavy batch of new year syndicated deals. The most prominent will probably be the new 30Y launch from Italy today. Other usual ‘early-movers’ (based on previous years’ deals) have failed to mandate banks so far. There is still time for the likes of Ireland, Austria, and Portugal to announce deals this week. If not, EUR rates will likely benefit from a temporary relief rally until next week.

Spain will add to syndicated sales with auctions of 2Y, 6Y and 15Y bonds, as well as linkers, and Germany will auction 10Y debt.

The US session will be no less lively with the release of December ADP employment and the minutes of the December FOMC meeting that saw the Fed accelerate its tapering and signal a much steeper pace of hikes this year.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more