Rates Spark: Let’s talk about rate cuts

Central banks bringing forward the date of the first hike also sees markets contemplating the prospect of subsequent cuts, something also visible on the US curve. The tone on European rates markets should remain understandably cautious, good omicron news or not.

Caution prevails in Europe

Good news relating to the severity of omicron should be taken with a pinch of salt. Faster transmission could offset the benefits of milder symptoms. More broadly, it is still early days, even if markets are starting to display omicron fatigue. As much as market reaction to adverse events can be violent, their attention span isn’t very long. What’s more, omicron or not, the reality of Europe’s Covid-19 wave means risk sentiment is likely to struggle to take off this side of the Atlantic.

Low EUR rates are storing up problems for later if inflation fails to fall in a hurry

Markets are starting to display omicron fatigue

This is particularly true in rates markets where year-end effects increase the gravitational pull lower for bond yields. European central banks have also shown signs of caution when it comes to taking the next tightening steps. Even if this only proves a short delay, the near-term impact is supportive of low bond yields in the coming weeks.

The FT was the latest to relay anonymous ECB members voicing their reluctance to make long-term commitments at next week's meeting. This is not the first such report and we would caution against focusing too much on the near term dovish reaction. The more important message in our view is the growing sense of unease about inflation overshoot, and the read-across from Fed policy to other central banks in Europe. Worse still, one of our fears at the onset of the omicron scare was that central banks would view it as another factor likely to push prices up. We have since heard officials from the Fed, BoE, and ECB voicing such concerns.

Hike means cut

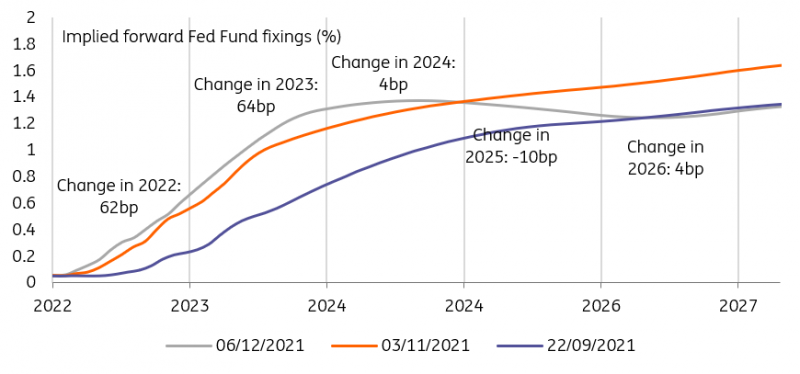

This cautious tone in Europe echoes the way markets have priced the recent Fed change of tack with regards to faster tapering. At face value, markets seem to heed the Fed’s hawkish warnings with higher short rates, but the curve is increasingly sending some concerning signals. Fed Fund forwards now imply that the Fed might cut rates in 2025 after raising them roughly five times. We are still far from markets pricing a full-blown policy error as it is routinely the case in central and easter Europe and the UK, but it shows concerns about the effects of Fed tapering.

Fed Fund forwards are pricing the possibility of a cut in 2025

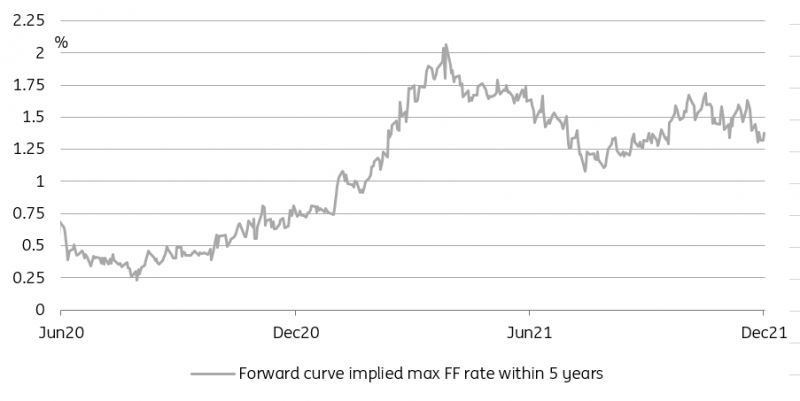

Note also that through phase of optimism and pessimism, markets have been relatively consistent in their estimation of the terminal rate, roughly 1.5%. If we take that value as a given, this means all Fed communication can do is affect the speed at which rates converge to this terminal rate. By this token, a faster hiking cycle should also bring forward the date of the next expected rate cut. This is what is happening on the USD curve.

A faster hiking cycle should also bring forward the date of the next expected rate cut

If this rate cut discount persists, or even worsens, it will display even more clearly investors’ scepticism that central banks can engage in a meaningful tightening. Next year offers a good chance of long-term rates rising back as a new balance between demand and supply for bonds is found after QE. Failing that, we’re looking at even flatter curves globally.

The market's estimation of the terminal rate has been surprisingly stable

Today’s events and market view

The main item on the calendar today is the release of the December Zew survey for December (yes, already). These surveys can have a market-moving impact despite their circularity (asking investors what their view is and then feeding the information back to investors). We think it remains a useful barometer of where consensus lies.

In comparison, the third release of the Eurozone Q3 GDP will feel a little more dated. The same goes for US Q3 unit labour costs. US Trade balance completes the list.

The most likely path is for rates to tread water globally, with a widening bias between USD on the one hand and EUR and GBP on the other if markets continue to take a benign view of Covid-19 developments.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more