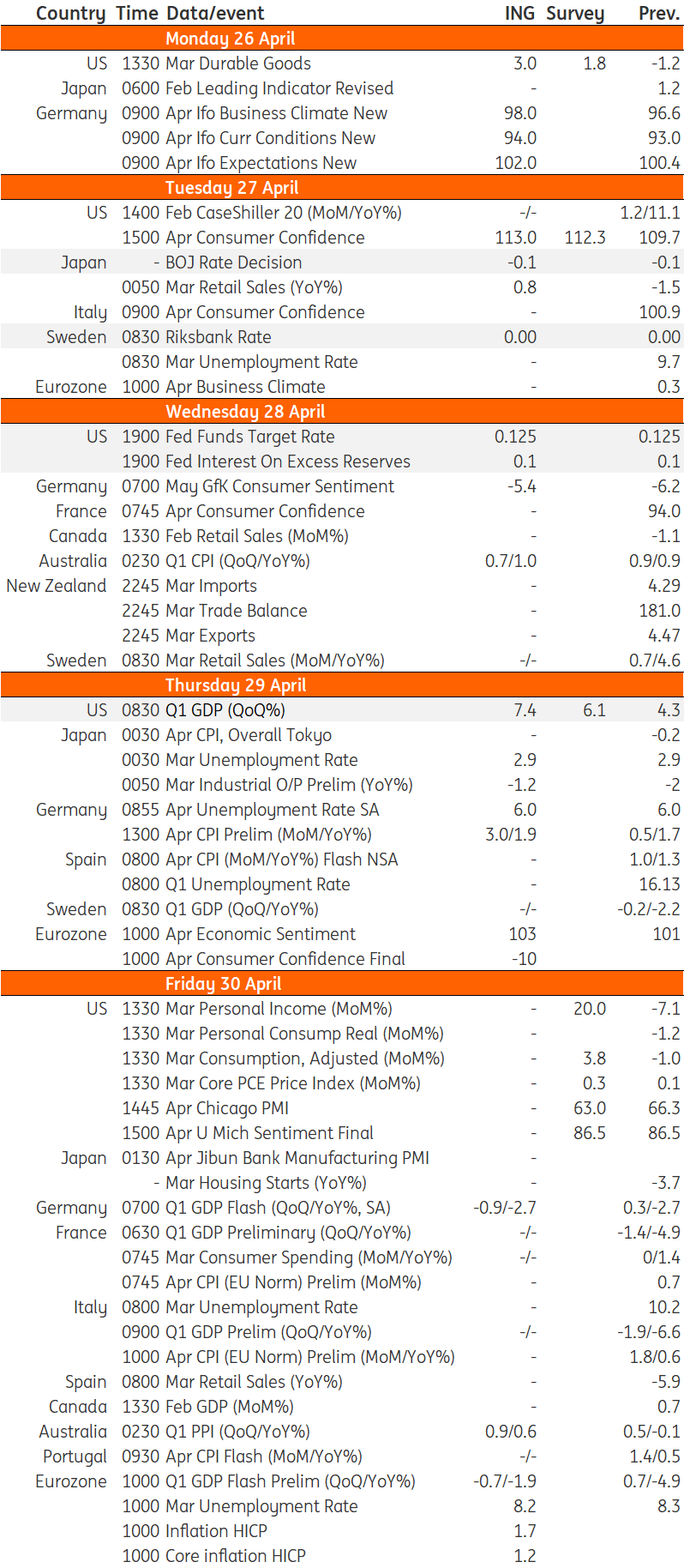

Key events in developed markets next week

We have a jam-packed calendar next week with central bank meetings in the US, Japan and Sweden as well as inflation, unemployment and GDP numbers from several developed countries

US: No change from the Fed but GDP figures to reflect vaccine optimism

It is a jam-packed calendar with the Federal Reserve monetary policy decision and the 1Q GDP report the highlights.

The Fed is set to leave monetary policy unchanged – rates remaining in the 0-0.25% range and QE monthly asset purchases at $120bn – with policymakers set to re-affirm there will be no shift in stance until “substantial further progress” on the recovery. Recent comments suggest that officials continue to think this is some way off, with the March forecast update suggesting that most members still think 2024 will be the start-point for lift-off in interest rates.

However, the 1Q GDP report is likely to show another fantastic growth figure, led by stimulus fueled consumer spending.

We are expecting annualised growth of 7.4%, and with the vaccination program meaning more than 135 million Americans have had at least one dose and the economy opening up more and more each day, we expect to see more than a million jobs created in April with GDP growth likely to be in double figures for the second quarter. With inflation likely to hit close to 4% and prove to be somewhat stickier than the Fed is publicly acknowledging – largely due to house price developments and ongoing supply capacity issues – we continue to think that the Fed could start tapering asset purchases before the end of the year.

We look for the first-rate hike to come in 1H 2023, but the odds are increasingly moving in the direction of a possible December 2022 rate hike.

Eurozone: A technical recession alongside energy price fuelled inflation

The eurozone is set for another technical recession, with numbers on Q1 coming out on Friday that will likely show another decline.

Extended lockdowns have pushed the economy in the red, even though underlying activity in sectors less hindered by restrictions seem to be performing well at the moment. Also interesting will be Friday’s inflation data set to soar further on the back of increasing energy prices. But we're not concerned, as all factors seem to be temporary, confirming the ECBs view laid out yesterday.

Also important is how unemployment performs; further falls will indicate a quick rebound on reopening.

Developed Markets Economic Calendar

Download

Download article23 April 2021

Our view on next week’s key events This bundle contains {bundle_entries}{/bundle_entries} articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more