JPY: Tweaking Kuroda

The Bank of Japan tweaked its unconventional policy artillery but the super-easy stance is still very much in place. Here's what it means for yields and the yen

JPY: BoJ’s subtle dovish policy tweaks keep a lid on JGB yields & JPY for now

When it comes to the July BoJ meeting, there was more to it than meets the eye – with the central bank making subtle, yet curious, tweaks to its unconventional policy artillery. But if anyone was in doubt, the super-easy BoJ policy is still very much in place; while officials will allow for greater flexibility in long-term yields, it’s important to stress the two-way flexibility here (not just upwards, but also downwards). In fact, by firmly restating the annual ¥80 trillion JGB purchase target, the BoJ is showing no real appetite for a rapid rise in long-term yields (there was an explicit aversion to this in the statement). What sealed the dovish deal was the guidance that the BoJ will "maintain very low rate levels for an extended period of time" – which is not too dissimilar to what the ECB stated last month. JGB yields declined as expected on a dovish BoJ, while USD/JPY price action has been choppy – albeit with the yen modestly lower as investors digest the news. We may see the pair drift up to 111.50-112.00 during BoJ Governor Haruhiko Kuroda’s press briefing. It’s clear, however, that BoJ tightening won’t be the catalyst to take the US 10-year yield back above 3%. That’ll be the job of US policy, with the Treasury yesterday upgrading its 3Q18 debt issuance (we’ll know tomorrow as to how they intend to raise this). A burgeoning fiscal deficit is one reason why we’re cautious on the USD over the medium-term. Watch also core PCE and 2Q ECI data today

EUR: Surprises in eurozone data will dictate near-term direction

It’s a busy day for key eurozone data releases – with both July CPI and 2Q18 GDP due (1100 CET). As ING’s Carsten Brzeski states, German inflation provided little evidence of a sustainable increase in underlying inflation, which leaves minimal hope for any positive inflation surprises in the eurozone-wide figure. Likewise, our economists do not expect the pace of eurozone GDP to have picked up – and pencil in 0.4% growth quarter on quarter. Look for EUR/USD to remain supported above 1.17 this week.

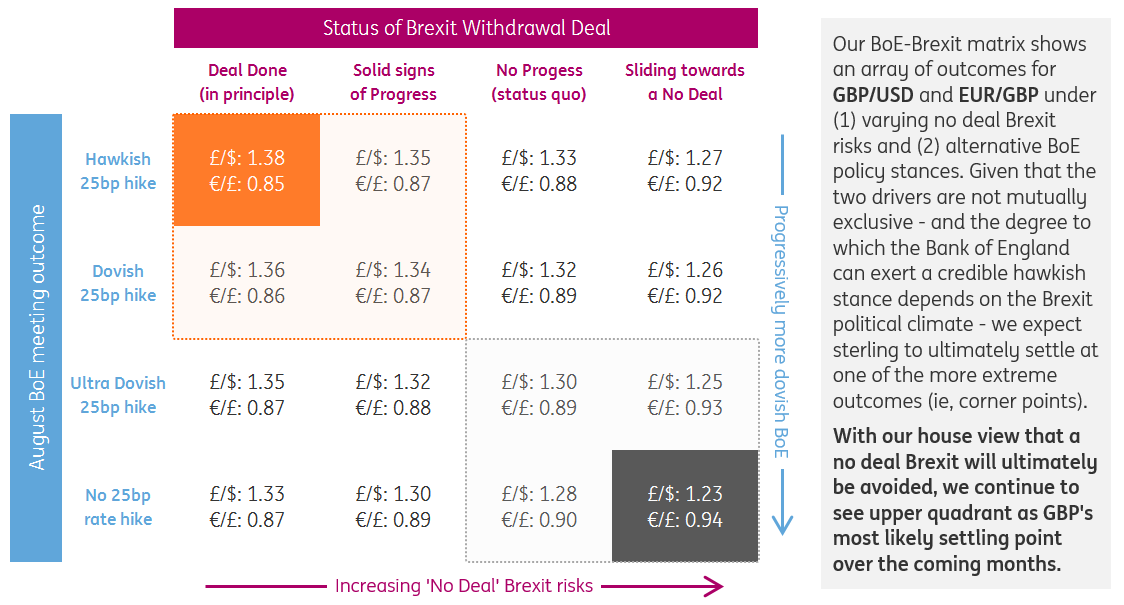

GBP: Not looking pretty as consumer confidence remains weak

GBP price action looks precarious going into Thursday’s August Bank of England meeting – with investors seemingly uninterested in a hawkish BoE hike. This seems about right to us, with the balance of risks pointing to limited GBP upside from what is likely to be a dovish BoE hike (see our GBP & BoE scenario analysis). More broadly, we see two factors driving GBP in the short-term – BoE policy and no-deal Brexit risks; given that they are not mutually exclusive, and the extent to which the BoE can exert a credible hawkish stance depends on the Brexit political climate, we see the GBP outlook becoming increasingly binary. While we may see GBP/USD test 1.30 – and EUR/GBP breach 0.90 – in the coming months, it’s worth reiterating that this short-term dip in GBP doesn’t mask the longer-term bullish potential. GBP/USD at 1.38 by the turn of the year may seem unlikely at this stage, but even a tiny amount of positive Brexit news can turn the pound’s fortunes on its head.

{kind=link}

CAD: Negative Nafta news may keep a buoyant loonie on the back foot

USD/CAD made a brief venture below 1.30 for the first time since mid-June. May GDP data today is expected to come in at +0.3% month on month (+2.3% year on year); any positive surprises could see a more sustained move sub-1.30 amid a mildly bearish US dollar backdrop. Reports that Canada has been excluded from Nafta talks between the US and Mexico may keep CAD on the back foot for now (and above 1.30).

"THINK Outside" is a collection of specially commissioned content from third-party sources, such as economic think-tanks and academic institutions, that ING deems reliable and from non-research departments within ING. ING Bank N.V. ("ING") uses these sources to expand the range of opinions you can find on the THINK website. Some of these sources are not the property of or managed by ING, and therefore ING cannot always guarantee the correctness, completeness, actuality and quality of such sources, nor the availability at any given time of the data and information provided, and ING cannot accept any liability in this respect, insofar as this is permissible pursuant to the applicable laws and regulations.

This publication does not necessarily reflect the ING house view. This publication has been prepared solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved.

ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam).