Macron v Le Pen: How markets could react to a far tighter election in 2022

The 2022 French presidential election campaign has many similarities to 2017, but also some notable differences. Rates markets' reaction should be more contained than then, as long as leaving the EU stays off the agenda. In FX, a risk premium is already visible in implied volatility ahead of the vote, but EUR/USD spot should be unaffected this year

Similarities, but mostly differences

In some ways, the French presidential elections scheduled for 8th and 23rd April 2022 may seem like a re-run of 2017: all the polls point to a second-round contest between Marine Le Pen and Emmanuel Macron, with Macron winning.

Yet, on closer inspection, the April 2022 election will be fundamentally different from that of 2017. First, the polls point to a much closer election result. 53% of the votes for Emmanuel Macron vs 47% for Marine Le Pen in the second round. So, a likely re-election then but one that's far from certain. In 2017 Macron won 66% of the vote.

Moreover, the context is fundamentally different. Macron (La République en Marche!) will no longer be at the head of a brand new party but will have to defend the record of his first mandate. And that mandate has been marked by social issues, notably the 'Yellow Vests' crisis and climate protests but also, and above all, by the covid crisis and its economic fallout. This has prevented him from implementing a whole series of reforms promised during his election, particularly with regard to the delicate issue of pensions.

Economic recovery and more optimism could help Macron perform better than polls currently suggest

Nevertheless, if, as we believe, the French and European economy rebounds strongly in the second half of 2021 and early 2022, in turn fostering optimism and confidence, the economic context could help Macron and make it much easier to defend his record. It is possible that Macron's current fragility in the polls is partly related to general discontent because of the Covid-19 crisis and the desire to send a warning. A context of economic recovery and more optimism could help Macron perform better than the polls currently suggest, notably by reducing the number of likely abstentions (which is set to be very high according to current polls).

| 47% |

Support for Le Pen in a presidential run-off against Macron in 2022Compared to 33.9% in 2017 |

A less aggressive strategy from the right

Marine Le Pen (Rassemblement National) will also be part of a completely different configuration. In 2017, her party had changed its name and was engaged in a campaign of 'de-demonising' the far right. Currently, the party seems to be less inclined towards an aggressive strategy and in a global context, that seems less promising, at both national and international levels. Indeed, at the national level, the issues of relocation and protection of strategic companies, usually favoured by nationalist candidates, has been addressed and defended by the entire French political class following the pandemic.

Internationally, nationalists seem to have less wind in their sails than in 2017

Internationally, nationalists seem to have less wind in their sails than in 2017, as evidenced by the defeat of Donald Trump and the rallying of Matteo Salvini to Mario Draghi's pro-European government in Italy.

Marine Le Pen will probably use the European difficulties of the vaccination campaign to support her nationalist message in her election campaign. However, it is not certain that this narrative will still have appeal in 2022 when herd immunity could well have been achieved and the economic recovery set to be well underway. This is probably why Le Pen is currently trying to position her party on issues other than her current favourite ones, namely security and immigration. Economic issues seem to have become more important in her statements, while promises such as leaving the EU and the euro have disappeared from her programme. The coming campaign will show whether this is a success or not.

A surprise in the first round cannot be ruled out

Even if all the polls currently point to a Macron-Le Pen run-off in the second round of the elections, it is still far too early to be certain about this outcome. The next few months will be crucial, as all parties unveil their candidates for the first round. One of these could still pull off a surprise and make it to the second round. Again, the differences with the 2017 election are significant.

If in 2017 the “Les Républicains” party had long-hoped to make it to the second round before judicial affairs caught up with François Fillon, their hope of making it to the second round is much lower for 2022. François Fillon has been sidelined and former president Nicolas Sarkozy has been caught up in serious legal troubles and convicted (the appeal procedure is underway). The only candidate currently known on the right is Xavier Bertrand, but the polls do not indicate that he has much chance of reaching the second round.

Some hope there will be one common candidate for the whole of the left

On the left, negotiations are underway, with some hoping to present one common candidate for the whole of the left (“Parti Socialiste”, “Europe Ecologie Les Verts” and Jean-Luc Mélenchon's “France Insoumise”). This possibility seems unlikely at the moment, as Mélenchon wants to run anyway and has a personality that is a bit too divisive to bring together the whole of the left-wing electorate. An alliance between the Greens and Socialists remains possible, with a single candidate who could be Yannick Jadot or Anne Hidalgo. However, even if the result of such an alliance would be better than the one obtained by the left in 2017, it would not allow the left alliance to reach the second round, according to the polls.

Ultimately, Emmanuel Macron seems capable of being re-elected in 2022 after defeating Marine Le Pen in the second round. He is currently trying to bring together the left and right strands of the electorate, via a climate and a global security law, and could be helped by an economic recovery. Nevertheless, the campaign has not really started yet, and recent French political history suggests that anything is possible. No scenario can be completely excluded. Social unrest, an epidemic rebound or too long a delay in the economic recovery could change the situation. European issues, notably the discussions on future budgetary rules, could also have a significant impact.

Rates markets: A more benign ‘Le spread’ with Frexit off the table

The run-up to the 2017 presidential vote saw some pretty dramatic price action in financial markets. It is worth looking back on these events to assess the likely reaction to next year’s vote.

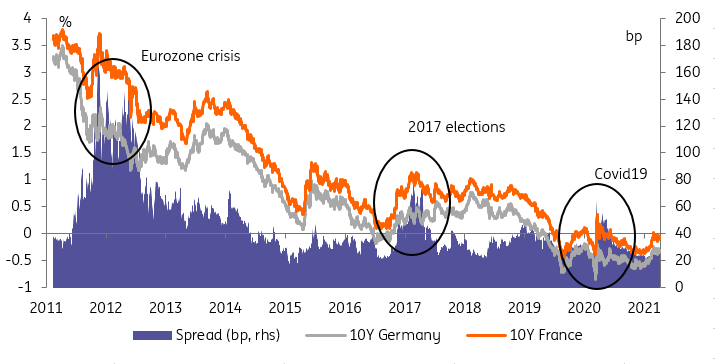

The main concern at the time, exemplified by the sharp widening of the 10Y Germany-France spread - jumping over 80bp, compared to a 5-year average of 33bp - was the risk of an exit from the EU and the eurozone. A Frexit.

Looking at the polls in the run-up to the vote, the risk of Le Pen, then a champion of Frexit, reaching the run-off was rightly deemed significant. More importantly in our view, the risk of two pro-Frexit candidates (Le Pen, far-right, and Mélenchon, far-left) making it to the run-off was deemed non-negligible. And indeed, Le Pen made it, and Mélenchon came a close fourth, with only 1.6 million fewer votes than Macron in the first round of voting. In other words, it was a close shave.

The 2017 election saw the second biggest jump in French spreads of the past 10 years.

Fast forward to 2021, Frexit has dropped off the agendas of both Le Pen and Mélenchon. In addition, while the former now stands an even better chance of making it to the run-off, Mélenchon is credited with less support than in 2017. We would not underplay how much of a shock a Le Pen victory would be for financial markets, but the seismic consequences of Frexit seem to be off the table.

We don't underplay how much of a shock a Le Pen victory would be for financial markets

We would not downplay the risk of a material increase in rates' volatility into next year’s vote and, in particular, in French spreads. For one thing, polls show that a Le Pen victory can no longer be dismissed out of hand. We have but a hazy idea of campaign platforms and themes this early before the vote but a long-time eurosceptic in the Élysée Palace would bode ill for future European integration. Also, by April 2022 bond markets won’t be able to count on support from the ECB’s main asset purchase programme, PEPP.

EUR: The French election risk a story for FX volatility for now but not for FX spot

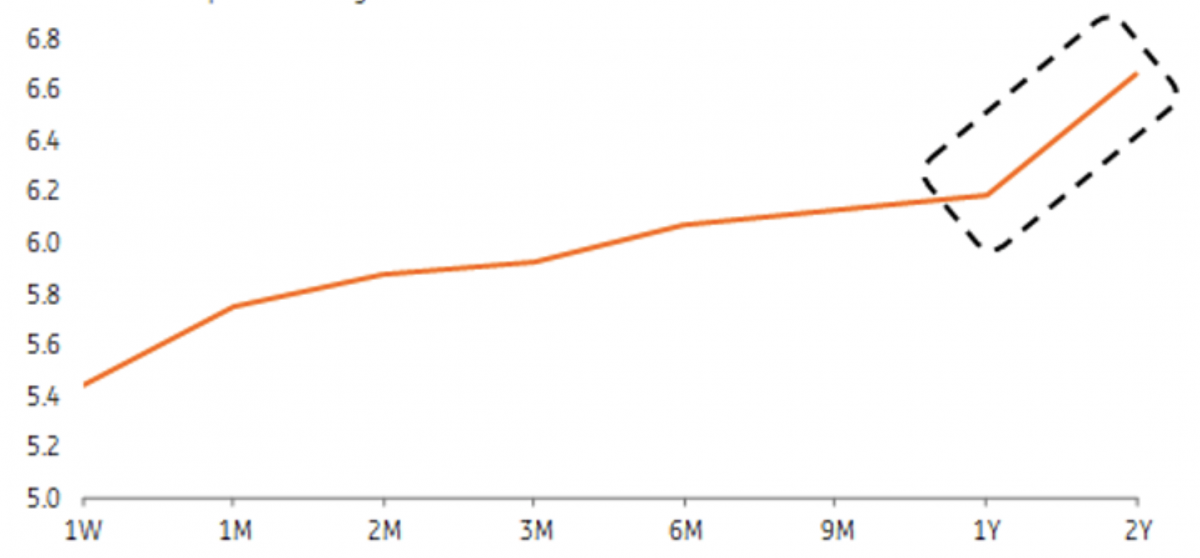

For now, we expect the spectre of the 2022 French presidential election risk to be rather a story for EUR/USD implied volatility markets than for the spot market. As our chart below shows, the EUR/USD implied volatility curve already exhibits a kink in the term structure around the April 2022 election date.

As for the EUR/USD spot, the prime driver for the coming months should be the road towards the expected summer eurozone economic recovery, helped by a faster vaccination process, the resulting improvement in poor eurozone activity data and the re-pricing of the bad news priced into the EUR/USD. This is evident in our short-term fair value model, which sees EUR/USD as undervalued by close to 2% at this point.

French presidential election risk premium already evident in EUR/USD implied volatility

EUR/USD ATM implied volatility term structure

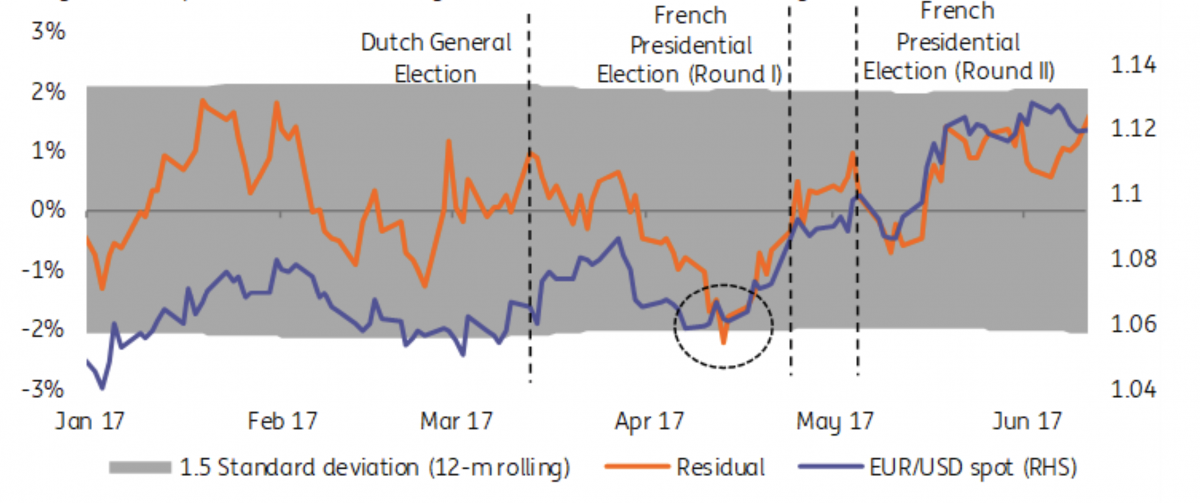

Using the same model, we gauge the amount of the risk premium built into the EUR/USD ahead of the French election in 2017. As you can see in our chart below, there was a meaningful risk premium ahead of the first round of the vote, with EUR/USD being more than 2% undervalued and trading outside its 1.5 standard deviation band. This is when market concerns peaked but, as it became apparent that Marcon was still likely to win, the risk premium got fully got priced out by the time of the first round – and EUR/USD jumped.

In 2017, the election risk premium was worth more than 2% in EUR/USD

Residual between EUR/USD financial fair value and spot. Large and persistent mis-valuation is a sign of a risk premium (as other things than normal drivers are affecting EUR/USD)

While the polls look much tighter now than back in 2017, things look set to improve in favour of the market-friendly candidate Macron by the time of the election; the economy should recover and the worst of the Covid situation should be over. That suggests that the EUR/USD risk premium ahead of the 2022 elections may not exceed that observed in 2017.

Importantly, the associated election risk premium in EUR/USD spot should be apparent in the cross much closer to the election date (in 2017, the French election risk premium started to be built into EUR/USD less than one month ahead of the event) rather than this year, allowing EUR/USD to focus on eventual positives this summer and the pair to move to the 1.25 level by summer.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more