Eurozone: Positive surprises

- 10 May 2019

Despite some better first-quarter growth figures, we don't think this marks the start of a new upward trend in economic activity. Throw in the fact that core inflation is likely to undershoot the 2% target over the next couple of years, and this suggests the ECB will stay put for the time being

Better growth figures, but not need to get overexcited

Looking at the latest data in the Eurozone, we can finally spot some reasons to be cheerful. According to Eurostat‘s flash estimate, the Eurozone’s GDP grew by a better than expected 0.4% in the first quarter or 1.2% year-on-year. Italy put in 0.2% GDP growth, thereby ending the technical recession that started in the third quarter of 2018. But there’s no need to get overexcited: while it is still very premature to pencil in a recession in Europe over the next 12 months, a significant growth acceleration shouldn’t be expected either.

The stronger than expected growth in the first quarter was probably helped by a normalisation of exceptional factors that held back growth in the second half of last year. But the first indicators for the second quarter cast some doubt that this growth rhythm can be maintained. Both the European Commission’s economic sentiment indicator and the PMI fell in April. The Eurocoin Indicator, a monthly proxy of the underlying growth pace, declined to a mere 0.18 last month, definitely not a sign that the expansion is accelerating.

Growth will remain slow, but recession risk is limited

To be sure, it is not that we see growth petering out in the coming months; there is still sufficient underlying momentum. Unemployment fell more than expected to 7.7% in March, underpinning consumption. We also believe the weakness in manufacturing is unlikely to last. The pick-up in China and some of the emerging markets should support European exports, though it might last until the third quarter before this effect really shows in the figures.

There is still sufficient underlying momentum

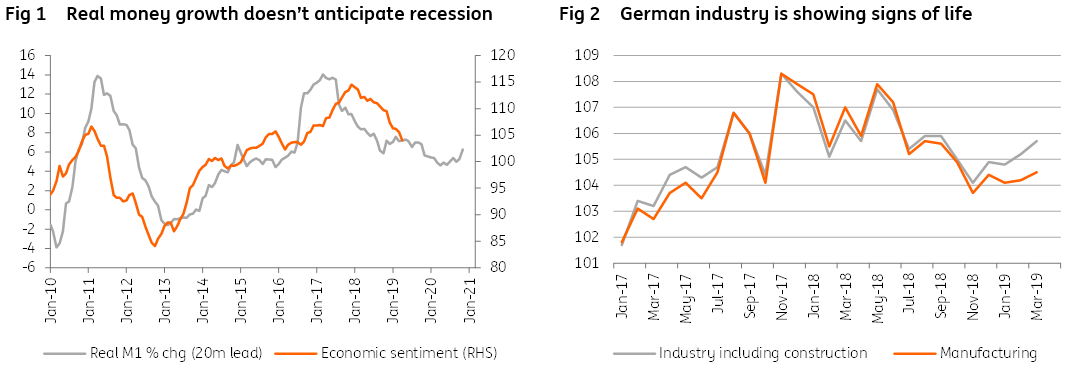

The fact that German industrial production increased by a stronger than expected 0.5% month-on-month in March, might already be a sign that industry is bottoming out. Growth of real narrow money, according to the ECB one of the best leading indicators of economic activity, clearly points to slow growth, but at the same time only limited recession risk up to the beginning of 2020. We are still comfortable with our GDP growth forecast of 1.2% both in 2019 and 2020, though 2021 might see a slowdown to only 0.9%.

European elections will be important

On the political front, the European elections might also be important for domestic reasons. The outcome in France will be seen as a poll on how the French react to President Macron’s reform proposals. In Italy, it will most likely show a strengthening of the League within the governing coalition, which could ultimately entice Matteo Salvini to trigger elections later this year to consolidate his strength. Italy is likely to see some renewed uncertainty anyway, as the European Commission already indicated a deterioration of Italian public finances, necessitating corrective measures in the 2020 budget.

We don't expect fireworks from the ECB

The inflation spike in April, with headline inflation jumping to 1.7% and core inflation to 1.2%, can be forgotten immediately. This is just a year-on-year glitch, caused by the late Easter holidays this year, pushing up hotel and package holiday prices. In May this should normalise again. We agree that the somewhat higher oil prices could push up inflation, but this impact is likely to remain muted. As for core inflation, a more reliable measure for underlying price dynamics, we don’t expect it to top 1.5% over the next two years, clearly undershooting the ECB’s inflation objective.

The ECB's change of tone has prompted speculation

The ECB’s change of tone has prompted speculation on new monetary initiatives. As such, the idea of a two-tiered deposit facility system was cheered by financial markets. However, ECB Board member Benoît Cœuré (picutred) poured cold water on the proposal by stating that there is no economic reason to do it, as so far the negative interest rate doesn’t seem to impact lending in member states with a high degree of excess liquidity. We, therefore, expect interest rates to remain stable over the forecast horizon.

That said, the ECB might want to use the new TLTROs to make small adjustments to the monetary policy stance over the next two years. Banks will be entitled to borrow up to 30% of the stock of eligible loans as at 28 February 2019 at a rate indexed to the interest rate on the main refinancing operations over the life of each operation. But there is no need to announce the same conditions for all upcoming TLTROs: conditions could be slightly tweaked according to the economic circumstances.

As for bond yields, we only see minor upward potential. While the halting of net purchases could trigger upward pressure, the expectations of short rates remaining low for a very long time and lower US bond yields in 2020 are likely to dampen this movement.

This article forms part of our Monthly Economic Update which you can find here

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

May economic update: Just when things were looking up

- This bundle contains 9 Articles