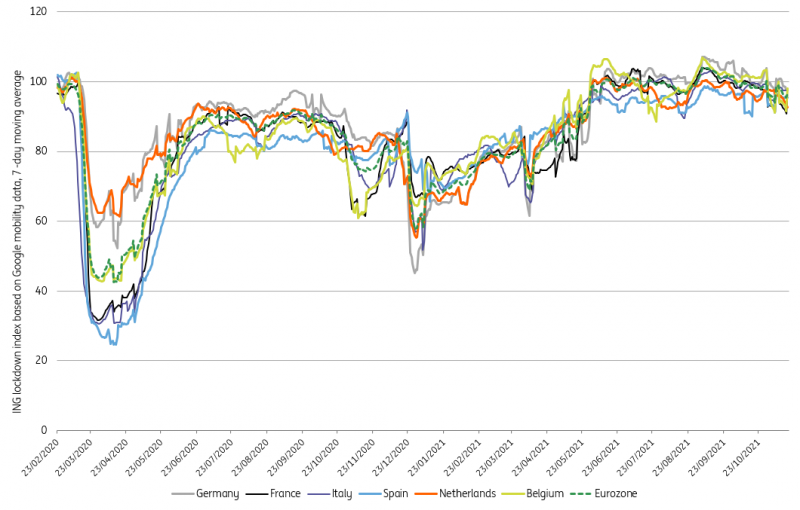

Eurozone mobility was already sliding ahead of new restrictive measures

Mobility in the eurozone started to slow down even before governments announced new Covid restrictions. Headwinds for the eurozone economy at the turn of the year have clearly increased

Mobility has already been on the decline, but marginally

As the next wave of Covid-19 is rapidly expanding across eurozone countries and the new Omicron variant has emerged as a new risk factor, concern that the pandemic will dominate winter are increasing. While vaccinations had initially reduced the ratio of hospitalisations, daily new cases have become so high that the impact on hospitals in several eurozone countries is rapidly becoming unsustainable. In Germany, for example, intensive care patients are already flown out to other regions to reduce the pressure on hospitals. With new lockdown measures being implemented or discussed, we want to take stock of the mobility impact of the wave so far.

Mobility has seen small declines so far across major eurozone economies

Mobility data from Google showed a steady increase until the end of the summer, with a turning point for the eurozone as a whole on 9 September. After that, we see a steady decline in daily trips to retail, grocery stores and leisure activities, while mobility at workplaces has held up relatively well. Despite the slowdown, activity is still higher than at any point during the summer of 2020 and comparable to late May 2021. This suggests that precautionary measures or voluntary changes in behaviour are still mild and that the fear of the virus is not yet very strong. However, even if it is modest, the decline in mobility so far adds to headwinds to GDP growth.

Most subcategories of mobility have seen similar paths of decline since late August

Restrictive measures set to cause a more noticeable slowdown though

Austria has led the eurozone before on measures fighting Covid-19 and it is doing so again this autumn. While other countries are still looking for other ways out, Austria has announced a strict lockdown to combat the rising coronavirus cases and hospitalisations, with non-essential shops, hospitality and leisure services being closed. With other countries experiencing fresh records in cases, it is likely that more restrictive measures are in the making for them as well, as mobility has hardly come down so far.

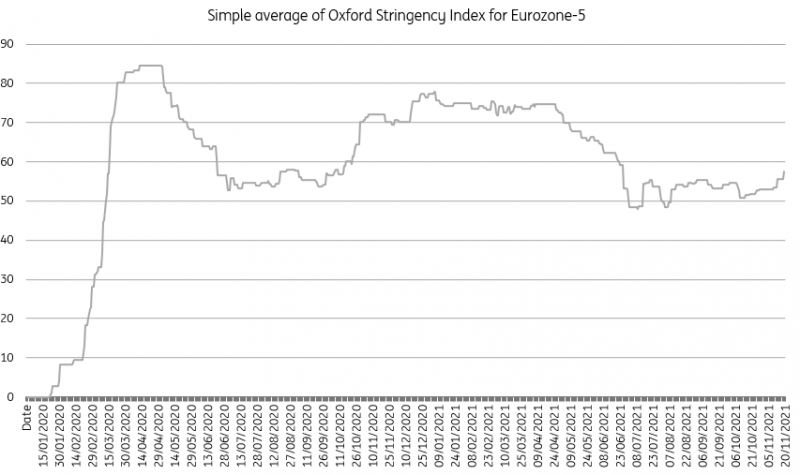

The second wave had a milder economic impact, but lasted much longer before restrictions eased

When looking at restrictive measures over time, we see that they have dramatically changed between waves. The first wave saw very restrictive lockdowns, which lasted just over a month before the easing of restrictions occurred. In the second wave, measures were more targeted and lasted much longer - about four and a half months on average for the five largest eurozone economies. In the first wave, this resulted in a steep drop in mobility of 56%. The second wave saw a decline of just 37%, which might still be overstated as some of the impact was felt over the holiday period when mobility would have been lower anyway. The economic impact of the latter was far milder and that makes the more targeted measures a likely option for governments for this winter. However, if the new Omicron variant turns out to be more contagious and aggressive, a return to the lockdowns of the first wave cannot be excluded.

The new Covid wave and the surge in infections adds to already existing headwinds like high energy prices and supply chain frictions. Many governments seem to have underestimated the potential of a fourth wave and insufficient vaccination ratios are currently backfiring. Thanks to vaccinations and the economy adjusting to measures over time, we still expect the damage from this Covid wave to be milder than in the winter of last year. However, with new restrictions and risks around the Omicron variant, it is deja-vu all over again. An unpleasant deja-vu, which suggests a clear hit to eurozone growth at the turn of the year.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more