The eurozone’s consumer’s still not putting their money where their mouth is

Eurozone consumption is still experiencing a temporary bump from catch-up spending on services although today’s PMI figures are already starting to cast doubt on that view. This summer might still see some relief but after that, a consumption slump seems in the making

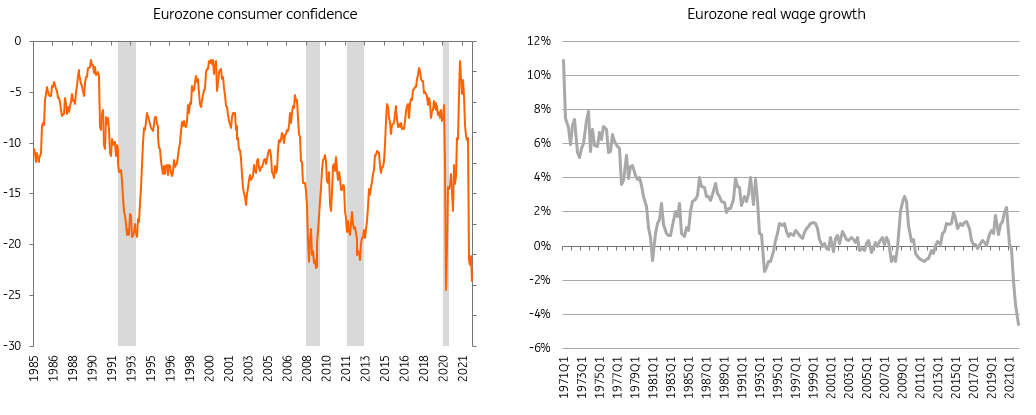

Consumer confidence is at recessionary levels

Since the start of the war in Ukraine, consumer confidence has dropped like a stone. Worries about the war, soaring inflation and a weakening economy cause uncertainty to return quickly among consumers. The drop in confidence has brought the eurozone back to levels last seen in the depth of the first lockdown and corresponds historically to recessionary levels as chart 1 shows. While every economic episode is different - and we wouldn’t dare base a recession call just on that chart alone - there are good reasons to expect a significant slowdown in household consumption on the back of the historic decline in real wages that the eurozone is currently experiencing (chart 2). With the first quarter already showing a decline in household consumption, is a consumer recession in the making?

Consumers are very gloomy as real wage growth reaches multi-decade low

Retail sales poor, but also just reverting back to trend?

Retail sales have been falling over recent months, with a peak in November 2021 after which sales have been on a choppy downward trend. It's understandable given the quickly eroding real wages, but we also have to note that sales had been above the pre-crisis trend for most of 2021 which can be explained by the inability to spend as much on services as consumers were used to (think of vacations, restaurants, etc.).

That leaves the question as to whether we are just reverting to the pre-crisis trend or whether weak sales are indicative of slowing consumption. Chart 3 shows that retail sales have developed below trend since late last year and April data suggest a further move down from trend. That suggests that the most recent developments show a weakening that goes beyond a simple correction to trend.

Retail sales have recently dropped below pre-crisis trend again

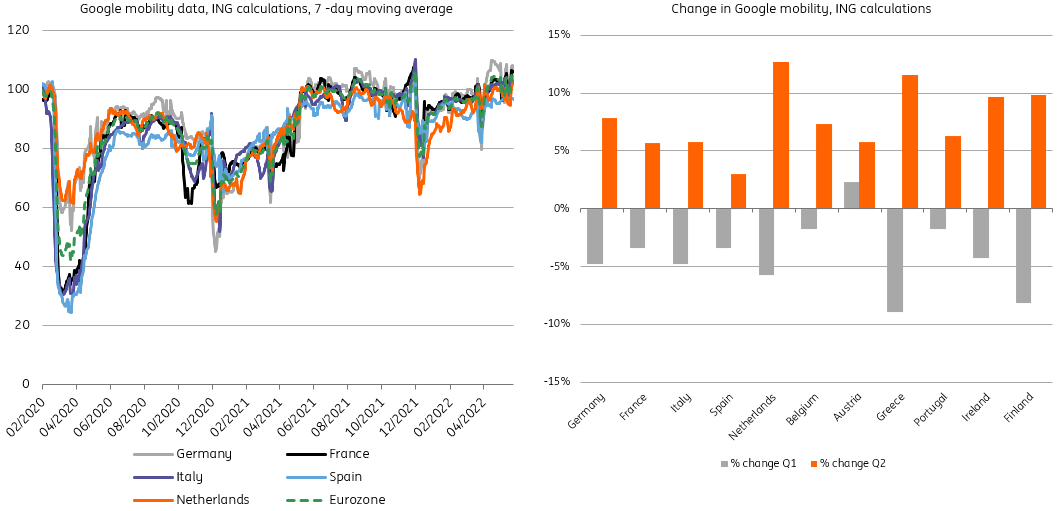

Mobility is looking favourable in 2Q thanks to the early 1Q Omicron dip

But while retail sales are currently disappointing, the economy is still profiting from reopening effects. Google mobility data suggest a continued rise in activity since January, which comes on the back of the winter dip in activity related to the Delta variant and the start of Omicron. A big caveat in this data relates to seasonal factors, as holidays have contributed to weak January activity. Regardless, the movement has been so favourable that this does confirm expectations of strengthening domestic economic activity. At this point, the eurozone is back above ‘normal’ in terms of daily movements to stores, recreation and workplaces, outperforming last year’s summer by just a little.

Mobility suggests that activity is on the rebound in 2Q

Reopening effects boost services activity

Thanks to the strong mobility data, it is important not to extrapolate retail sales to total consumption at this point. Services consumption, especially tourism-related activities, have vigorously rebounded as corona restrictions and fear of the virus have been falling. This results in a shift in spending that could play out favourably for consumption in the second quarter and possibly the summer.

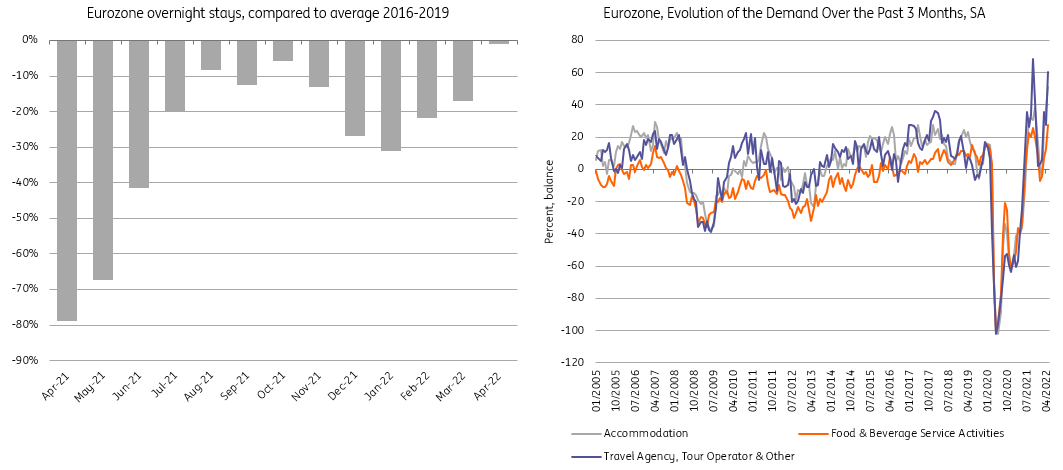

After two years of missing out on holidays abroad or going to restaurants and bars, people seem eager to catch up on lost time and may be looking less at their bank accounts due to the exceptional circumstances of recent years. There is little current data to go on, but overnight stays have been rapidly catching up in most eurozone economies while survey data suggests very strong activity in the travel, hospitality and accommodation sectors. That indicates that eurozone consumption has experienced a sizeable tailwind from reopening effects, even if actual restrictions have already been eased quite a while ago. Today’s PMI figures for services do suggest slowing growth in these consumer-related services though, so the question is now how long these tailwinds can last.

Consumer services are rebounding after two years of pandemic

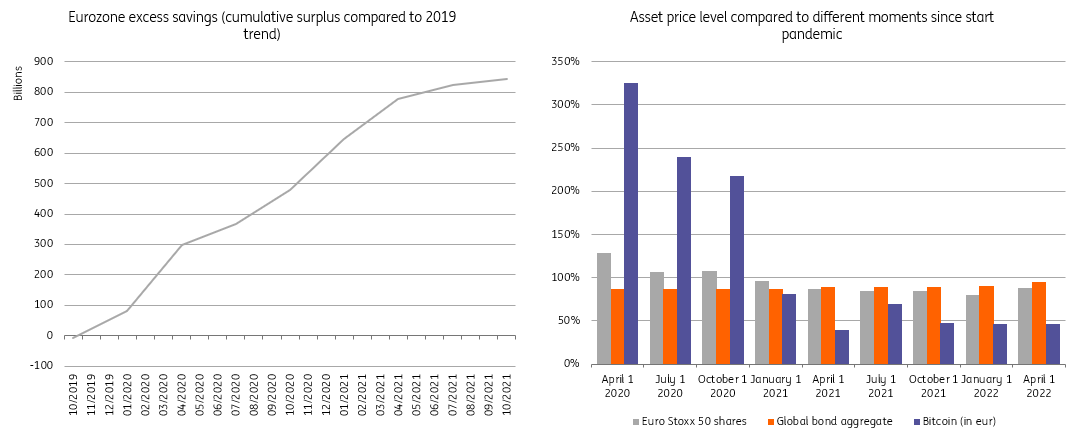

Excess savings from the pandemic are rapidly eroding

With a weak June services PMI, the question becomes more important as to how long this reopening effect can continue. The main wildcard for continued strong spending, while real wages plummet, comes from savings. The pandemic saw an unprecedented runup in the savings rate, which has resulted in large excess savings. Savings figures go up to the fourth quarter of 2021 so far, which means that the latest data is still missing, but even if savings haven’t been run down so far, they have taken a serious hit.

The inflation rate will evaporate significant parts of it and besides that, assets have taken a beating. Retail investors have flocked to stock and crypto markets to invest some of the excess savings they had, which have recently dropped significantly.

Savings have increased, but dropping asset prices and high inflation erode potential

Besides that, savings seem to have been accumulated mainly by higher income groups, which are groups that generally have a lower marginal propensity to spend. That means that the upside to how much will flow back into the economy will be limited. All in all, with savings having been eroded by inflation and losses on investments, together with the unfavourable distribution among income groups, it does not look like we can count on continued elevated spending for much longer.

Consumption seems to be having its last hurrah

The message around domestic consumption in the eurozone seems complicated at the moment. Bleak confidence figures and historical declines in real wages suggest that households are set to consume less. At the same time, relaxing behaviour related to the coronavirus is still giving the economy a short-term boost with mainly tourism-related spending performing very well. This is also reflected in much stronger mobility data, generally correlated with improving domestic economic activity.

Consumers are able to spend a little extra in part due to improved savings over the course of the pandemic, but this is limited due to falling asset prices and lopsided savings over income groups. That means that weak consumption is around the corner. A strong tourism season could boost it until the summer, but sluggish consumption, at least, is set to kick in after that.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more