EUR and ECB Crib Sheet: Hawkish expectations may be unwarranted

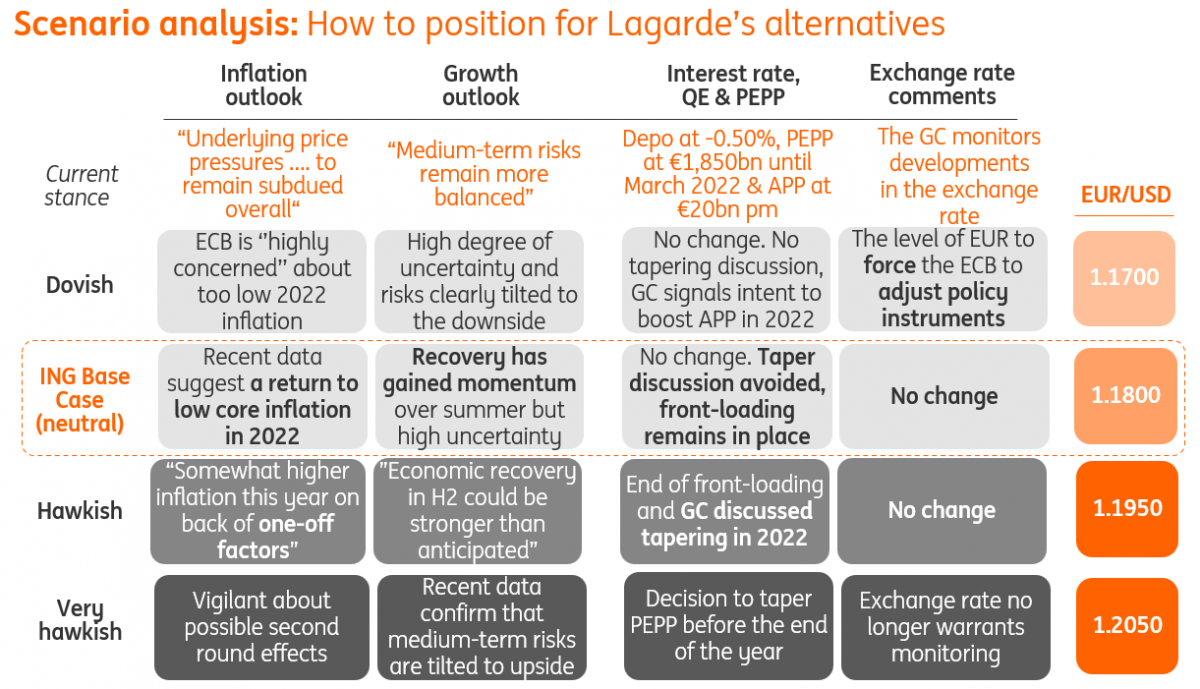

Recent price action suggests that the market has turned slightly more hawkish on the ECB, all to the benefit of the euro. However, we doubt that the ECB will provide any hawkish hints through tapering (front-loading of purchases should remain in place, in our view) or through the inflation forecasts. In turn, the EUR could give up some of its recent gains

ECB may fail to meet hawkish market expectations

The market has recently turned more doubtful about the ability of the ECB to retain an ultra-dovish stance and keep postponing the tapering discussion, especially after another rise in the eurozone’s inflation and some hawkish members voicing their concerns about excessive monetary stimulus.

In FX, such developments provided the first idiosyncratic push to the EUR, after a long period where EUR/USD was, by and large, a mirror of the dollar’s dynamics. We suspect that, in order to continue reaping all the benefits from the softer dollar environment, the euro will likely need to receive some hints from the ECB this week that the tapering discussion is underway. But, as highlighted in our ECB meeting preview, we suspect that the Governing Council will try to keep any tapering speculation at bay and should refrain from ending the front-loading of asset purchases – which would likely be interpreted as a de-facto tapering.

Considering that the expectations embedded in the EUR ahead of this week’s ECB meeting are likely more skewed to the hawkish side than in previous instances, we think there is room for EUR/USD to give up some recent gains if our expectations for a still very cautious stance - which should also be reflected in broadly unchanged inflation forecasts for 2022 and 2023 - prove correct. Still, it appears that the options market is not pricing in much higher than normal volatility around the meeting. The break-even on a straddle (which is a bet on higher volatility) on Thursday is currently 27 pips.

EUR/USD may stay in the 1.17/1.20 range during fall

Also in the longer-run, we think the ECB will trail the Fed on tapering, both on the communication side and on the time/pace of asset-purchase reduction. From an FX perspective, this should make the EUR default to a condition where it struggles to take fully advantage of periods of stabilisation in global risk sentiment and the dollar, as we expect markets to mostly reward those currencies that can count on the prospect of domestic monetary tightening/normalization.

For the rest of the 2021, we expect EUR/USD to trade within the 1.17/1.20 range, with the possibility of the pair moving to the upper bound of the range at the end of the year when the dollar is seasonally weaker. As the start of the Fed’s tightening cycle draws closer, we think EUR/USD will enter a downward trend in 2022.

Read our latest FX views in the September FX Talking

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more