ECB removes the free lunch from banks

- 27 October 2022

- Financial Institutions

The ECB is changing the terms of the TLTRO-III bank funding operation from November. The cost of participating will become higher. Sticking to funds makes sense for funding purposes, in our view. We expect repayments to edge up but are mostly supported by existing liquidity reserves. Refinancing via bond markets makes little economic sense

The European Central Bank (ECB) announced changes to the terms of the targeted longer-term refinancing operations (TLTRO)-III programme in its October meeting. From 23 November 2022, and until maturity or early repayment date, the TLTRO interest rate will be indexed to the average applicable key ECB interest rates over this period. The ECB offers three new voluntary early repayment dates starting 23 November. The cost of the TLTRO tranches for banks that have met the lending benchmarks will move to at least 1.5% after 23 November (to the level of the deposit rate as of 2 November), but the level for the remainder of any tranche will most likely be higher than this as the ECB continues to hike rates. Until 23 November, these banks enjoy the very attractive rates based on the average of the operation until November.

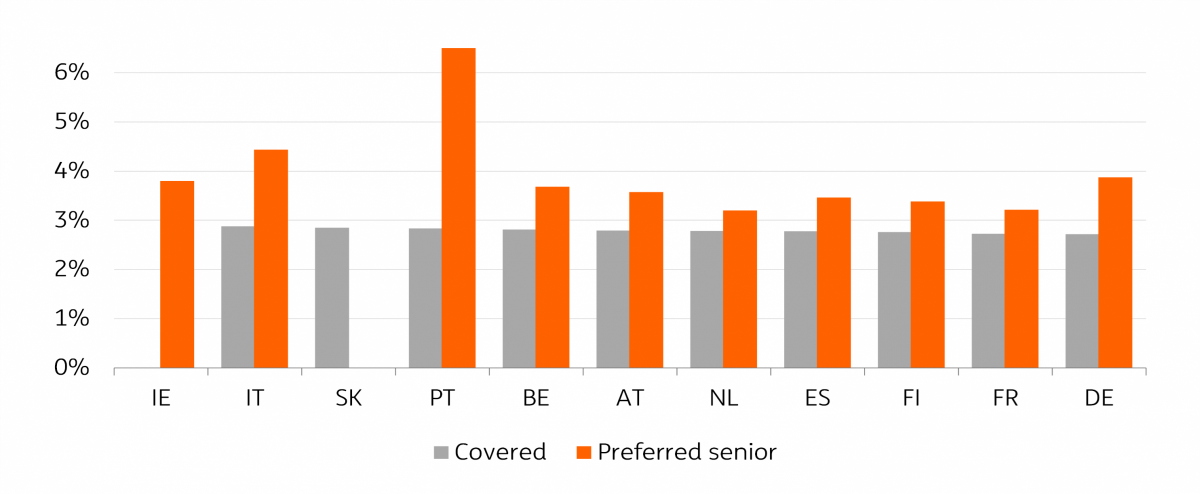

While the cost of the operation will become higher for banks, the levels compare relatively attractively with bond market yields due to the substantial repricing of underlying interest rates this year. Most covered instruments trade with yields closer to 2.8% in the 2024 maturity bucket, while preferred senior is quoted even at higher yield levels than this (around >3.6%). Thus, while the ECB has changed the conditions, we don’t think the change will result in massive early repayments for banks that use the operations for funding. Instead, these banks are likely to remain more cautious, especially considering the substantial volatility in the financial markets and worries over the economic outlook. For banks that have drawn funds more opportunistically, the question is less straightforward. While you can continue depositing the funds back at the deposit rate to the ECB, the TLTRO drawings have a negative impact on MREL (minimum requirement for own funds and eligible liabilities) or leverage ratio metrics. For these banks, a quicker repayment may thus seem more attractive.

We think that stronger banks may utilise early repayment options to drive down, at least partly, their excessive TLTRO drawings. This can perhaps also be used as a signal to the markets that the liquidity buffers are at strong levels allowing for the action. Smaller or lower-rated banks are unlikely to be able to refinance the drawings at competitive rates via bond markets. For these, repaying early does not make sense.

Covered and preferred senior unsecured bond yields for 2024 maturities

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more