Dutch pension funds continue adding interest rate hedges

- 19 June 2025

- Rates

Dutch pension reforms can leave a significant mark on rate markets, especially at the longer end of the curve. Overall, we expect an unwind of longer-dated swaps upon transitioning, but until the transition date, funds will want to keep interest risks hedged. The latest data confirms that funds are continuing to add to their interest rate hedges for now

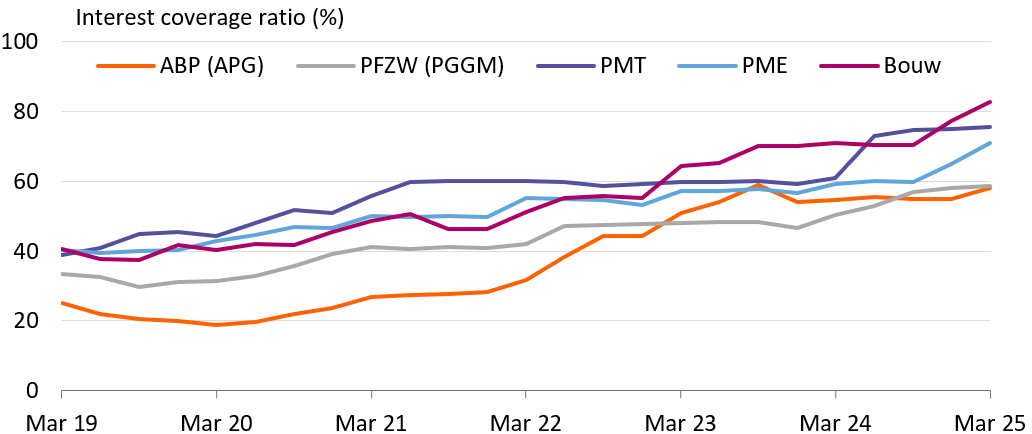

Dutch pension funds continued to add to their interest rate hedging

The latest data from this year's first quarter shows that the five largest Dutch pension funds all increased their interest coverage ratios. The pension fund for the construction sector, Bouw – with roughly €80bn in assets under management (AUM) – even edged above 80% with its coverage ratio. Bouw cites higher interest rate hedging of its buffer as a driver of the increase.

The further rise in hedges is in line with our expectations, as pension funds will want to derisk in preparation for the transition dates on 1 January 2026 and 2027. Having said that, we do find the size of the increases for funds like Bouw and PME notable. ABP and PFZW are the largest two funds (of around €800bn), and if these decide to follow this trend, we can still expect a strong demand for fixed receivers going forward.

Demand for interest rate hedges remains strong

Healthy funding ratios keep up the need of shorter-dated hedges upon transitioning

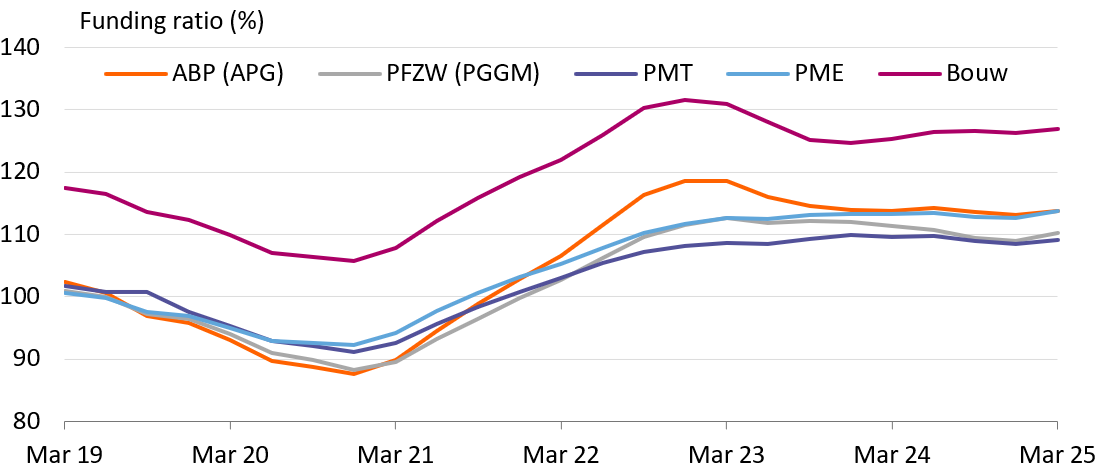

Funding ratios have improved in the first quarter (see chart below), supported by higher interest rates and decent equity returns. Liberation Day came just after the close of the quarter, so we can expect a slight worsening from that point onward. If trade tensions trigger another leg lower in 20Y rates and a sell-off in equities, we could see funding ratios falling again. Having said that, for now, funds seem in a good position to transition.

On the transition date, any funding ratio excess (above c.105%) will be allocated to each participant's individual pot. In effect, that would mean that those in retirement would suddenly see an increase in their pension payments. In the new system, most funds will hedge such liabilities by close to 100%, which is likely higher than the current overall hedging ratio. As such, a higher funding ratio on the transition date could imply a demand for shorter-dated hedges.

For younger participants, however, a higher funding ratio is unlikely to change the demand for interest rate hedges too much. These longer-dated exposures will no longer need the same amount of interest rate hedging from a regulatory perspective compared to the old system, and funds will therefore likely still have to reduce their longer-dated hedges.

Pension funds benefited from rising rates and higher equities

Recent delays highlight the challenges to a smooth reform period

Two smaller funds (Fysiotherapeuten & Dierenartsen) just withdrew from their intended transition date on 1 July 2025. The administrative side of the operations was said to be insufficient for guaranteeing a smooth transition. The funds notified their participants just two weeks before the transition date, which underlines the uncertainty markets are still facing when it comes to timing flows.

Of the biggest funds, PFZW, PMT and Bouw still target 1 January 2026. A possible last-minute change can lead to a surprise in markets, especially given the large flows anticipated upon transitioning. As such, any pre-emptive steepening of the 10s30s curve is at risk of reversing on headlines of delays.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more