Covid-19 and the eurozone economies in 2021: Darkest before dawn?

The eurozone economy will continue to be dominated by the coronavirus, much as in 2020. Optimism prevails for the latter part of the year though as vaccinations are expected to boost economic recovery. Don’t expect the ECB to remove support quickly though

With lockdowns extended into the new year, it really feels like it is darkest before dawn in the eurozone. In the first quarter, GDP is all but certain to contract again and the question is now by how much. Vaccination programmes have started off slowly, but are expected to pick up speed once teething troubles are smoothed out. We expect the combination of lockdowns and vaccinations will allow for more substantial reopening of economies over the course of the second quarter. This will then also mark the start of the recovery of the eurozone economy.

The recovery will pick up steam once vaccinations are more widespread and the virus retreats more permanently. For the second half of the year, that will likely result in a strong growth recovery, further boosted by the Recovery and Resilience Fund that will start to disburse grants to EU countries. This will coincide with a period of stronger inflation, which is partly mechanical. Energy inflation will be higher on the back of a reversal of the oil price decline seen in March last year and the German VAT decrease of last year is not renewed. Social distancing price categories are also likely to make up for discounts given during coronavirus times, which makes a temporary surge to around 2% a possible scenario.

The ECB is not expected to reduce support quickly as the economy recovers. While inflation could temporarily tick higher, the ECB is focused on the medium-term inflation outlook for its policy making and the medium-term outlook is not improving much. In fact, with unemployment trending somewhat higher and output gaps very negative, it is likely that it will take longer than expected pre-crisis before inflation is sustainably returning to just below 2%. The pandemic emergency purchase programme (PEPP) has already been announced to run until spring 2022 and early tapering is unlikely to become a theme for this year. There is huge uncertainty surrounding this base case though, which makes it worth looking at other possible scenarios as well. Given the importance of vaccine rollouts and lockdowns for the economy, those are the drivers of the various scenarios we look at.

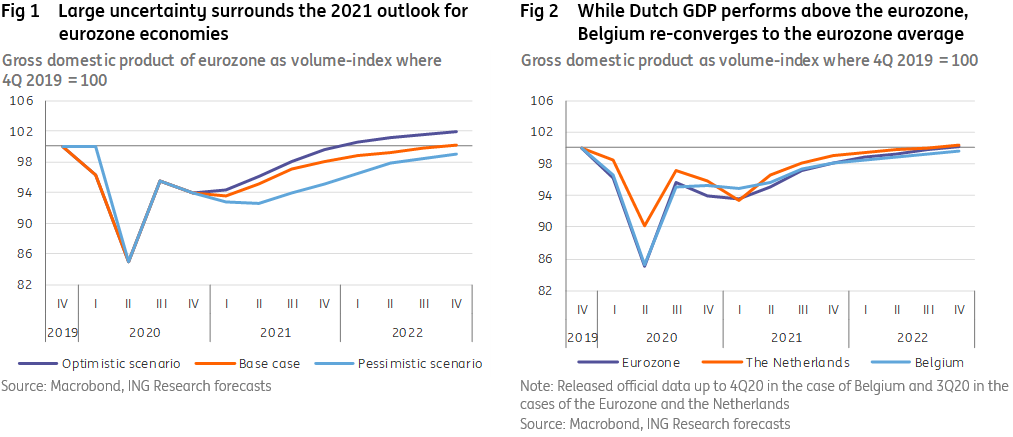

- A more optimistic take would be one in which lockdowns succeed in bringing down new cases very substantially and improved testing capability compared to the first wave allows new cases to be kept at a very low level. This, together with a speeding up of vaccination efforts that inoculates the vulnerable population within a matter of weeks, would lead to an aggressive reopening of the economy and could lead to 4.1% GDP growth for the year.

- A downside scenario that we look at is one in which mutations of the virus require longer and stricter lockdowns that last well into the first half of the year and still impact summer holidays substantially. Thanks to mutations, roll-out of vaccines takes longer due to required adjustments and this delays herd immunity until 2022 or later. In this scenario, GDP growth would drop to just 0.9% for the year.

The Netherlands: higher volatility, but more resilience

Like other eurozone economies, the Dutch economy took a big blow from the Covid-19 crisis, leading to a GDP decline of roughly 4% for 2020. However, with a below-eurozone-average contraction in the first half of the year (-9.9%) and an unexpectedly strong rebound in the third quarter to 97% of the pre-crisis peak of the fourth quarter of 2019, the Dutch economy had a relatively favourable GDP performance during the bulk of last year. This was probably related to a combination of the comparatively looser “intelligent lockdown”, the effectiveness of discretionary fiscal support policies and size of automatic stabilisers, a favourable sector composition (tourism is relatively small), an above-average digital infrastructure together with a large share of the economy that does work that can be done from home (such as business services).

We project negative growth for the Dutch economy, while the Eurozone GDP stays flat and the Belgian economy already starts to rebound compared to the fourth quarter

As in Belgium, the number of Dutch Covid-19 cases started to rise again in the autumn, earlier than in the rest of Europe. While this resulted in a significant peak of cases in October in Belgium, the Netherlands kept the curve flatter but for much longer. The high level of novel cases around Christmas, which has been coming down gradually since, and the return to lockdown mid-December translates into a negative GDP growth for the fourth quarter in 2020 and a below-average first quarter of 2021. In fact, we project negative growth for the Dutch economy, while the Eurozone GDP stays flat and the Belgian economy already starts to rebound compared to the fourth quarter. We assume that the strict lockdown will end in the first quarter in the Netherlands, with only a gradual unwinding of social distancing measures. Even though the Netherlands will be a long way off herd immunity by then, the second quarter of 2021 should see increased levels of mobility and a GDP rebound to a level close to but still below that of the third quarter of 2020.

Even though the current Dutch second lockdown is stricter than the first that started in March 2020, GDP seems to be holding up somewhat better now, for a number of reasons:

- Businesses are better prepared with new business models (such as restaurants switching to home deliveries) and are dealing with less uncertainty, given that many fiscal support instruments were already in place and automatically fluctuate with a firm’s turnover.

- Consumers are more used to online shopping and businesses have their distribution channels more in order.

- Manufacturing is holding up better, facing fewer input supply restrictions from, for example, China.

- As a trading nation, the Netherlands is benefiting from the recovery of world trade. While service exports are still weak, goods exports are higher than before the crisis hit.

Given the resilience shown after the opening of the first lockdown, we assume a strong rebound mid-2021 as well, which might be facilitated by the substantial presence of flexible relations in the Dutch labour market. In our pessimistic scenario, in which the virus calls for more caution and the vaccination process remains slow, economic activity might be more suppressed in the first half of the year, only to start a slow gradual recovery in the second half of the year.

Dutch public finances were in good shape going into the crisis, with debt levels much lower than the eurozone average and Belgium. Only after the January 2021 announcement of additional support for the first two quarters of 2021 is Dutch debt expected to go above the European norm of 60% of GDP. In light of new elections, the reforms that would be required and the ease of financing its own debt, the current government decided not to apply for support from the European Recovery Fund yet. Elections for the Dutch House of Representatives are to be held on 17 March, which might bring about some uncertainties. Current polls suggest that the majority of the electorate supports the parties making up the current coalition government, even though it stepped down prematurely because of the so called “childcare allowance” affair. Given the likelihood of a high number of parties, probably four at least, involved in the process of forming a new government, we expect it to take longer than the historical average of 94 days to install the new government.

We expect it to take longer than the historical average of 94 days to install the new government

Positive for the economy is the fact that opposition parties have given the caretaker government ample room to handle the Covid-19 crisis, even though on other controversial topics the government will refrain from taking new initiatives. This also means there is room for more fiscal stimulus, if deemed necessary.

All in all, we project the Dutch economy to rebound somewhat stronger than the eurozone and Belgium, possibly with a bit more volatility at the start of the year.

Belgium: in the middle of the pack

Although Belgium was very hard hit by the pandemic in 2020 (it still has one of the highest mortality rates in the world due to the pandemic), the economic impact was within the European average. With a GDP contraction of around -6.2%%, the situation in 2020 is worse than in Germany (-5%), but better than in France (probably -8.3%). In particular, it should be pointed out that the rebound in the economy in the third quarter, when the restrictive measures were eased, was surprisingly strong. The fact that German industry performed well in the second half of the year probably played in favour of Belgian exporters during that period.

This being said, Belgium also stands out for its very large second wave of the pandemic (larger than the first) which hit the country early (as early as October). As a result, the authorities had to take drastic measures to curb the pandemic, and to do so more forcefully than most other European governments. Most of these measures are still in force today and will probably be in force until March. In the face of the upsurge of cases in many countries, it can be seen that many have more recently taken the same type of measures. For the first quarter of this year, as in the Eurozone, we do not anticipate a recovery.

As in most eurozone countries, assuming that there are no nasty surprises in the vaccination process, we expect the recovery to gain traction over the course of the second quarter. The second half of the year should also be marked by an acceleration in activity.

Compared to the scenario for the eurozone as a whole, we will nevertheless pay attention to three elements:

- The situation of Belgian public finances was among the worst at the start of the crisis. Since the situation has deteriorated sharply, the room for manoeuvre for financing a recovery plan will be narrower than in most other euro area countries. This could weaken the recovery path in the coming years. Admittedly, the European Recovery Fund should grant some €6billion to Belgium. But more will be needed to get the economy back on track.

- Moreover, we know that once the urgency of the pandemic has passed, political tensions may take over. It should be remembered that it took 17 months to form a federal government. It now brings together no fewer than 4 political families, sometimes with diametrically opposed ideas. Questions about economic recovery and its financing in a difficult fiscal framework risk exacerbating the tensions already present.

- Lastly, given the very high degree of openness of the economy, the recovery path will also depend on the global economic context and the economic health of Belgium's main trading partners. This may have a positive effect on growth, for example if Germany succeeds in strongly reviving its activity. But it can also have a negative effect, for example if protectionism continues to rise. The presence of many multinationals will also have to be monitored; major restructurings impacting the Belgian sites of multinationals have already been announced, which could make the labour market deteriorate more than in other countries.

In conclusion, we believe that Belgium will not be far from the trajectory of the eurozone. But it will not be at the head of the pack.

Download

Download article6 February 2021

BNLX+ Financials: Fasten your seatbelts This bundle contains {bundle_entries}{/bundle_entries} articles

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more