We’re downgrading China’s growth and currency as challenges mount

Widespread flooding, tough social-distancing measures at ports, chip shortages and far tighter regulation in some industries - these are all big challenges facing the Chinese economy right now. New and traditional infrastructure projects could provide a lifeline. Nevertheless, we're downgrading our GDP and USD/CNY forecasts

A particularly challenging third quarter

Let me give you just a snapshot of some of the big problems China is facing right now. In July, the major city of Zhengzhou suffered from serious flooding. Zhengzhou is known for its smartphones and semiconductor production. The floods hit factory operations and intensified chip shortages. As a result, we can expect higher prices for our hand-held devices.

A month later, China suspended some sea and air freight around Shanghai due to a new breakout of Covid-19. This resulted in major congestion affecting the import of commodities and the exports of goods and parts. We don't expect things to ease there until late September to October. The result will be increased global freight prices which could have a knock-on effect for goods in the west.

On top of that, we have reforms the government is implementing in various parts of the economy. We'll discuss those later. But you can start to see why we're downgrading our China GDP growth figures and revising our USD/CNY forecasts.

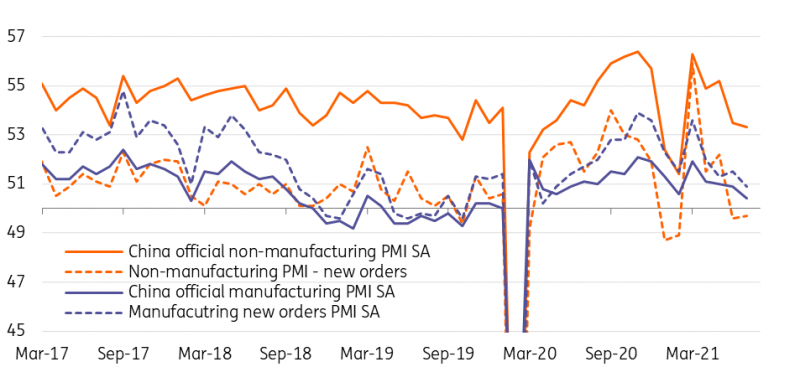

China PMIs show activities slowing

Consumption weakness is likely to continue

Covid-19's localised social distancing measures are likely to continue into next year as new variants emerge. But there's more. The Chinese government has recently announced a clampdown on the technology and education sectors. This is now putting pressure on the job market and subsequently consumption growth.

Clampdowns are putting pressure on jobs and consumption

Last month, private education centres were banned from making a profit. This is an industry worth around $100bn a year. We don't have exact figures on the numbers of people who lost their jobs but we could be looking at 90,000 in the Beijing area alone. You can read more about this here.

The question is whether the young people in this industry will be able to earn as much as they did before; it's unlikely. Spending from this group will therefore be lower on items from rent to high-end consumer goods.

We do not think this is the end of this round of regulatory tightening. More reforms may be aimed at boosting the productivity of the younger generation, for instance by encouraging them to spend less time on smartphones and so on. We also expect there'll be changes to the allocation of school places and disconnection from where students actually live. That in turn will affect house prices.

China retail sales online vs shops

Semiconductor chips are key to manufacturing growth as is the technology war

Chip shortages will continue to affect factory output growth. This is already evident in automobile investment, production and sales. And it's becoming apparent in other sophisticated electronic goods which have many chips in just the one product such as production equipment and smartphones.

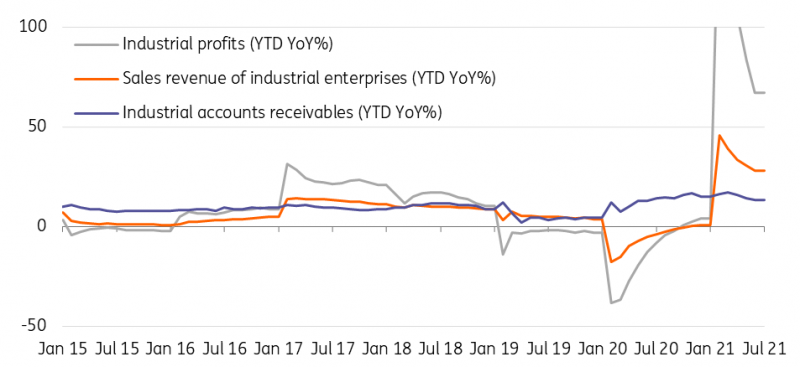

This does not necessarily mean slower profit growth for manufacturers. Chip prices have gone up on a year-on-year basis as have the prices of the products that use the most chips. This might be the explanation for higher industrial profits, besides low base effects, helping industrial profit growth to jump above 50% year-to-date, year-on-year.

The main risk is the delay to 5G infrastructure work globally

The main risk is the delay to 5G infrastructure work globally from reduced tax revenues and fewer available workers due to Covid. This could result in smaller orders of semiconductors received by factories.

The “technology war” is another risk for China's manufacturing sector as the US has increased the number of Chinese companies on its entity list.

President Xi has tasked Liu He, the Vice-Premier, with leading the advancement of technology, especially semiconductor chips which shows just how important this goal is. But there will be no immediate results. Fiscal support for technological advancement will first go into investment rather than production.

China industrial profits are strong due to negative base effect

Fiscal policy to support infrastructure projects, the engine of GDP growth

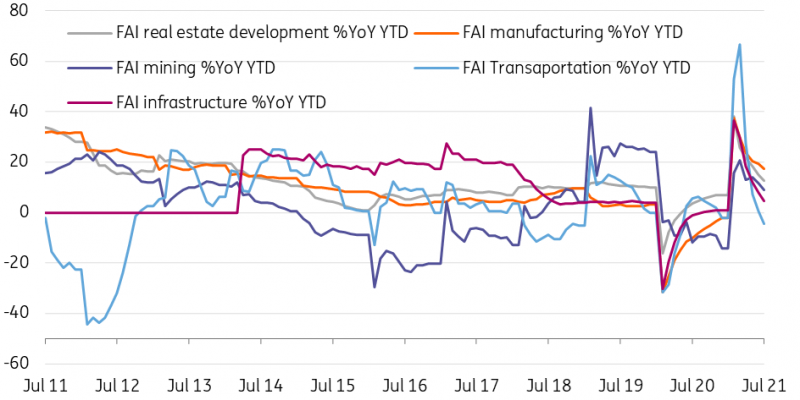

Fixed asset investment has slowed. There are several reasons for this. The first is that local government debt issuance has reduced as credit costs have increased in China's bond markets. This has led to a lack of funding for some infrastructure projects. Another is that some industries face challenges to get hold of semiconductors and therefore have no appetite to increase production capacity. This includes automobiles and telecommunication infrastructure. Both have experienced contractions in fixed-asset investment.

The central government will try to accelerate infrastructure projects to support economic growth

We expect that the central government will try to accelerate infrastructure projects to support economic growth. But this needs direct financial support from the central government as we expect some local governments will still face high credit costs, delaying their bond issuance.

Infrastructure in China means “new infra” as well as “traditional infra”. Both are treated as important growth engines by the Chinese government. For new infra, China has yet to complete the coverage of its 5G network. For traditional infra, China has many planned projects for railways and highways to link up cities across provinces. To achieve a reduction in carbon emissions, China also needs to build more solar and wind electricity generators.

Infrastructure will be the stabiliser of Chinese growth.

Infrastructure and transportation investments have been slow

ESG is getting more important - green, common prosperity, corporate governance

Environmental: Achieving net-zero carbon emission.

China is fine-tuning the momentum of its carbon reduction so that we do not see a repeat of the spikes in commodity prices such as we saw with the PPI subindex for coal and coking, which rose from 3.7%YoY at the end of 2020 to 45%YoY in July. The National Development and Reform Commission revealed that some coal mines have resumed production, returning capacity of 667 billion tonnes per year. Some other coal mines can operate for one more year to smooth out the price spike. The coal mine example tells us that the Chinese government is balancing the reduction of carbon emissions with the rise in energy prices. We expect that the action points to achieve peak carbon in 2030 should be released soon. Regulations should be clearer for the energy market by then. China is completely serious about achieving net-zero carbon emissions by 2060. And anti-pollution policies should be expected in all industries, especially for medium to highly polluting industries.

Social: Common prosperity, what does it mean?

President Xi has mentioned common prosperity recently. There are many media reports on this, and most have focused on the introduction of a national property tax. In fact, we think it will be a lot broader than that. Property taxes are only one of the taxes that redistribute wealth from the rich to the poor. More big corporations are going to set up social responsibility funds if they have yet to do so, and the size of donations from them should increase. The tax curve, for individuals and for companies, should become more progressive, with higher rates of tax for those who earn more. This is not unfamiliar to the western world where many countries apply a similar taxation system. People and companies in rural areas will benefit from this "common prosperity" concept. This is not simple to implement. The distribution of tax revenues between local governments and the central government is always awkward. Reforms on sharing tax revenues between local governments and the central government have been studied, but decisions have not yet been made. Now, the common prosperity concept might break existing rules. But we still have to wait and see what the details will be.

Governance: Corporate governance is key to avoid regulatory trouble

Corporates need to take bigger steps to enhance their corporate governance and social responsibility. They need to work to get ahead of the regulators. There are many things that could increase costs to corporates, including control of data storage, employee benefits, and how their products could affect national policies, like the third child policy. In the short term, this means expansion of teams in corporate governance and in the long term means the costs of doing business in China will increase.

Monetary policy

Credit costs are going to increase with policy risks and the weaker economic momentum from the chip shortage and Covid. If some infrastructure projects have to rely on the issuance of local government bonds then the government should have an intention to lower bond yields.

To achieve this, the central bank, PBoC, can cut the Required Reserve Ratio (RRR) by 0.5 percentage points in the fourth quarter of this year. The RRR cut in July has shown that this policy action is successful in bringing down market lending rates, not just those at banks, but also bond yields.

I once worried that the RRR cut would be a too aggressive loosening of monetary policy. But the economy has obviously slowed down which now make another RRR cut more likely. And the need for a policy interest rate cut of 7D reverse repo, 1Y Medium-lending facility rate (MLF rate) 1Y Loan Prime Rate (LPR) looks unnecessary if the RRR cut can serve the same purpose.

GDP growth and USDCNY forecasts

Combining the risks and the opportunities, we have scaled down our GDP growth forecasts for the second half of 2021. Chip shortages and Covid are the two main reasons. We expect GDP growth to slow to 4.5%YoY and 5.0%YoY in 3Q21 and 4Q21, respectively, with the full-year forecast of 8.9%, down from 9.2% back in July.

With weaker growth, we expect monetary policy in China to diverge from that of the US, resulting in a narrower interest rate spread. Following this, capital inflows could slow or even experience a small reversal. We forecast USDCNY to reach 6.7 by the end of the year from the estimate of 6.45 made in July.

Download

Download article

25 August 2021

Good MornING Asia - 25 August 2021 This bundle contains {bundle_entries}{/bundle_entries} articles"THINK Outside" is a collection of specially commissioned content from third-party sources, such as economic think-tanks and academic institutions, that ING deems reliable and from non-research departments within ING. ING Bank N.V. ("ING") uses these sources to expand the range of opinions you can find on the THINK website. Some of these sources are not the property of or managed by ING, and therefore ING cannot always guarantee the correctness, completeness, actuality and quality of such sources, nor the availability at any given time of the data and information provided, and ING cannot accept any liability in this respect, insofar as this is permissible pursuant to the applicable laws and regulations.

This publication does not necessarily reflect the ING house view. This publication has been prepared solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved.

ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam).