CAD: Ready, but still not cleared, for takeoff

Covid-19 and a generally-strong dollar are set to limit USD/CAD downside for now, although the loonie is still likely to outperform the more China-exposed Australian dollar and New Zealand dollar. In the longer-term CAD has all the cards in order (above all, an attractive carry) to be the key G10 outperformer once risk aversion dissipates

USD/CAD still supported by Covid-19 in the short-term

Since the end of 1H19, USD/CAD has oscillated in the 1.30/1.33 band, primarily stirred by global risk dynamics. Trade tensions seemed to have paved the way for a period of benign risk environment for the loonie but the Covid-19 outbreak then came to haunt high-beta currencies – whilst providing safe-haven support to the dollar.

The virus inevitably poses a significant downside risk to the loonie, at least in the short-term. Apart from being strictly reliant on a supportive risk environment, CAD presents the highest correlation in G10 with crude oil prices (Figure 1).

Figure 1 - CAD the most exposed to oil in G-10

Our commodities team has recently revised down their oil forecasts (Figure 2) and noted that this is not only related to the coronavirus-induced demand woes but also to the uncertainty around OPEC+ interventionism to support crude prices. Pressure by Saudi Arabia to cut production more – in line with the OPEC recommendations – are being challenged by Russia’s reluctance. Our new forecasts for oil embed the view that prices should remain depressed in the short term and possibly into 2Q.

Loonie less vulnerable than antipodeans

All this suggests that, as long as the coronavirus story keeps market sentiment in check, USD/CAD will be unable to enter any sustained downtrend. However, CAD should continue to outperform the rest of the $-bloc currencies (AUD and NZD), as it has looser ties to the Chinese economy and is therefore relatively less vulnerable.

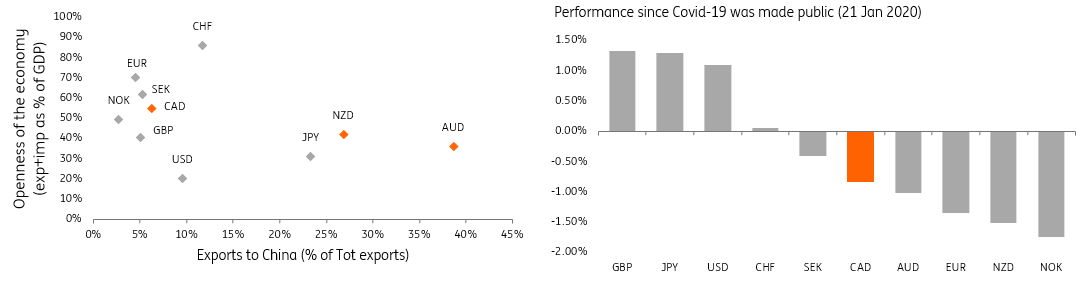

Figure 2 shows how Canada, compared to Australia and New Zealand, is an equally open economy but relies way less on exports to China (shown in the x-axis).

Figures 2 & 3 - CAD exposure to Covid-19 is smaller than its peers

In Figure 3, the performance is calculated on a trade weighted basis (source: BIS)

These differences have been acknowledged by the market, as proven by the outperformance of CAD to the other currencies since the inception of Covid-19 (Figure 3). It must also be noted that both the RBA and RBNZ delivered hawkish messages after the outbreak, which sizably reduced the downside for AUD and NZD. Looking ahead, once more evidence of a Chinese slowdown accumulates and starts to bite into domestic data of the exposed countries, the more protected Canadian economy should allow CAD resilience vs the G-10 risk-sensitive to remain well in place.

CAD is well positioned for a rebound in sentiment

Estimating how long Covid-19 will keep markets on a defensive stance is a hard task, and we cannot exclude the negative spillovers on risks will last for numerous weeks. However, it seems reasonable to expect that by 2H20 fears of a global pandemic will have dissipated and the environment for risk-related currencies will be less adverse.

With this in mind, it is worth looking at what currencies are best positioned for a rally once risk sentiment recovers. Figure 3 shows how CAD has the most attractive 3-month risk-adjusted within the G10 space at the moment.

Figure 4 - CAD: the best carry in town

We still have a rate cut by the Bank of Canada in our forecast, mostly on the back on the uncertain external backdrop and as the Fed may still take a step to ease. However, the economic backdrop has improved with the most recent data-flow.

In particular, the latest jobs report showed a jump in wage growth (along with a drop in unemployment), which endorses the notion that inflation is unlikely to stir materially below the BoC target band mid-point (2%) anytime soon.

All considered, even if the BoC ultimately delivers a one-off insurance cut (on the back of external risks), this will hardly be able to severely dent the CAD rate advantage. Incidentally, markets would not be particularly prone to price in further cuts as the inflation backdrop should remain solid. This leads us to believe that the loonie will likely be one of investors' top choices to enter carry trades once risk sentiment stabilizes.

We expect USD/CAD to remain relatively supported in the short-term and as long as coronavirus fears keep markets jittery. However, CAD remains set to outperform its peers AUD and NZD thanks to a less exposed economy to the prospect of a Chinese activity slowdown.

Looking beyond, we expect CAD to lead the rebound in risk-sensitive currencies thanks to its highly attractive carry, even if the BoC delivers a one-off insurance cut. We expect USD/CAD at 1.26 in 4Q20, with most of the downturn likely materializing towards the second half of the year, when a recovery in oil prices and the dollar starting to retract from recent highs should assist the carry-driven CAD rally.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more