Bank of England: Why we don’t expect a rate cut this month

It's a close call, but a recent post-election pick up in sentiment should be enough to see the Bank of England avoid cutting interest rates this month

Markets are primed for a UK rate cut

There’s a week to go until the Bank of England announces its first decision of the decade, and markets are gearing up for an interest rate cut. Swap pricing suggests a 60% probability of easing next week (30 January).

We’re less convinced and think policymakers are more likely to ‘wait-and-see’ how the recent uptick in sentiment translates into activity before deciding on action – although it is undoubtedly a close call.

Either way, here’s our attempt to get inside the heads of the committee as they begin their deliberations.

Four versus Five - the doves still just about outnumbered at the Bank of England?

As the nine committee members take their seats around the table, we know all four of the ‘external’ MPC members are tempted to cut interest rates.

After all, two have already voted for easing at the previous two meetings, and the other two - Silvana Tenreyro and Jan Vlieghe – have both used recent speeches/interviews to hint they could join the rate cut camp too.

We think policymakers are more likely to ‘wait-and-see’

However, it’s not clear that the remaining five ‘internal’ members of the committee will back calls for easing right now. Admittedly, we don’t have that much to go on in terms of communication, but as we noted at the time, our sense from Governor Mark Carney’s recent speech was that he hadn’t been fully convinced of the merits of cutting interest rates this month.

While his comments were perhaps the most candid he has been on the idea of easing, he noted the better news on politics, and pushed back on the idea that the Bank was running out of ammunition.

So will the views of the five 'internal' members have changed since then?

The case for keeping rates on hold

Well, in the November report, and again in December, policymakers summarised their views as following (our emphasis):

“UK GDP growth was projected to pick up from current below-potential rates, supported by the reduction of Brexit-related uncertainties, an easing of fiscal policy and a modest recovery in global growth. With demand growth outstripping the subdued pace of supply growth, excess demand and domestic inflationary pressures were expected to build gradually”.

On global growth, our trade team argues that the recent US-China deal is unlikely to do much to improve world trade volumes. But the recent truce does at least mean that the situation for global activity hasn’t worsened significantly since the Bank of England last made its forecasts in November.

Likewise there’s nothing yet to force a change in the Bank’s view on fiscal policy, although admittedly the jury is still out on which of the government’s pre-election promises will be included in the forthcoming budget.

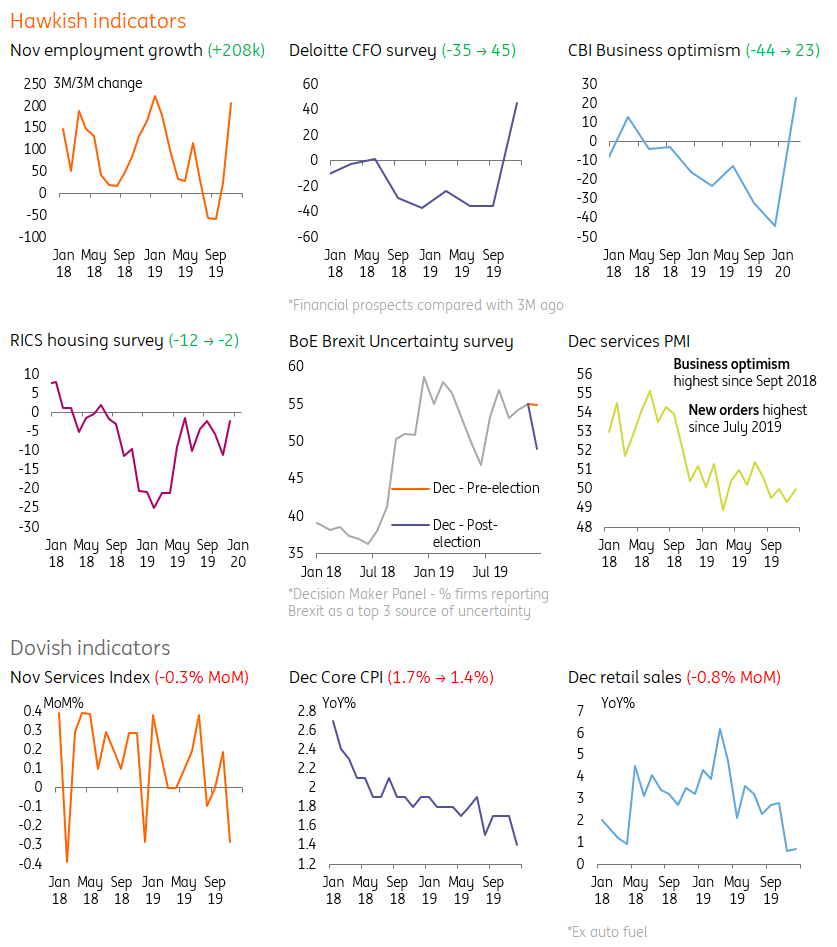

So as ever, it all comes down to the impact of Brexit uncertainty on the economy – and here the news looks good. Sentiment data – including the Bank’s own Decision Maker Panel – has virtually all painted an improved picture. Most are pointing to renewed optimism and increased demand.

Sentiment data has virtually all painted an improved picture

And despite some disappointing headline figures, we aren’t convinced the hard data has got much worse either. While the retail backdrop was undoubtedly dreadful over the festive season, the weak consumer story isn’t especially new – and if anything the fundamental wage/inflation backdrop points to a slight improvement in the new year.

The recent pick up in employment data also suggests the jobs market is performing more resiliently than hiring indicators had been indicating over the final few months of 2019.

How the figures have stacked up since December

The case for cutting interest rates

So far so good, then? Well, not completely. We think there are two good reasons to doubt the recent improvement in sentiment related to Brexit.

Firstly, sentiment indicators aren’t always great performers at political turning points. Generally survey-based measures are given as diffusion indices, that is they tell us how many respondents are thinking something has improved, but not by how much. Economists (including the BoE) learnt this lesson back in 2016 when the PMIs plunged, prompting an easing package, only to rebound the following month.

There’s a risk that business optimism starts falling again as the reality of UK-EU trade negotiations hits

Incidentally, that's why we think markets may be getting a bit too excited about the January PMI figures due Friday - while they are likely to show an improvement, policymakers will treat them with a certain degree of caution. We suspect they'll be paying closer attention to what in-house agents are learning anecdotally from businesses.

Secondly – and more importantly – there’s a risk that business optimism starts falling again as the reality of UK-EU trade negotiations hits. Don’t forget that since the election, most now assume the transition period will not be extended, and at best, a bare-bones free-trade agreement covering goods will be agreed this year.

That potentially means plenty of changes to the way firms operate internationally (both for goods and services), and while there’s plenty of uncertainty over how companies will react to these changes in advance, it’s unlikely to spur a wave of longer-term investment.

Our verdict

While we are somewhat sceptical about the recent rise in sentiment data, and aren't convinced we'll see a big increase in investment post-election, we think the Bank of England will opt against cutting interest rates this month.

After all, the MPC decided against moving in November and December following a pronounced deterioration in the 'soft' data, and the case in favour of easing hasn't increased significantly since then.

We suspect we're likely to get either a 6-3 or 5-4 vote in favour of keeping rates on hold when the Bank announces its decision next week.

Of course that is still fairly close, so we certainly wouldn't rule out easing. If we were to put a totally unscientific probability on the chances of a cut this month, we'd say perhaps 30-35%.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more