Bank of Canada set for lift-off

We look for the Bank of Canada to raise interest rates 25bp on 26 Jan. Activity is strong, the economy is seeing record employment and inflation is at 30-year highs. Covid containment measures are also set to be eased at the end of the month and this should signal the green light to hike rates. Expect a positive impact on CAD, although external risks are mounting

Strong economic recovery boosts the case for action

The Bank of Canada cut rates to 0.25% and initiated a C$5bn per week asset purchase programme in support of the economy as Covid containment measures were brought in to stem the pandemic. As the economy recovered, the Bank of Canada was among the first to start pulling back on the stimulus by tapering the asset purchases down to C$4bn per week in late 2020, before going to $3bn in April 2021 and C$2bn in July 2021. Asset purchases were then abruptly concluded last October with maturing assets reinvested, thus maintaining the size of the balance sheet.

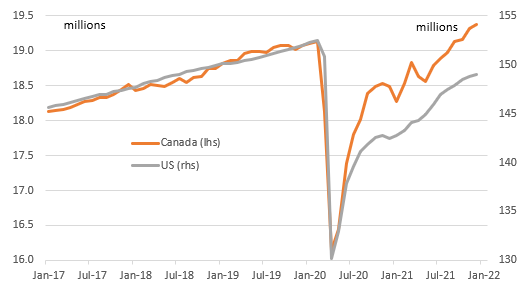

Since then, the economy has battled both the Delta and the Omicron waves, but has continued to add jobs in impressive numbers. The chart below shows that the Canadian jobs market has performed far more impressively than that of the US. In fact, employment is now at a record level of 19.4mn with the unemployment rate back below 6% even though the economy, as of the third quarter, was still 1.4% smaller than in 4Q 2019. This lost output will soon be recovered with the latest Bank of Canada’ 4Q Business Outlook Survey reporting sentiment at a record high as companies highlighted a “broadening recovery in demand”. Notably, investment and hiring intentions are at record highs, which is consistent with our own GDP forecast of 3.5% for 2022 after 4.5% in 2021.

Employment levels (millions)

Inflation and easing restrictions gives BOC the green light

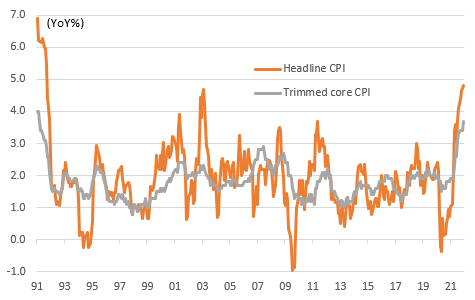

At the same time, inflation is on the up with prices rising at their fastest rate for more than 30 years. The same BoC survey suggests no let-up in inflation pressures anytime soon with respondents saying they expect supply disruptions through the second half of 2022 while labour shortages are constraining output. In this environment where the economic outlook is robust, the jobs market is red hot and inflation is at generational highs, we see little reason for the BoC to delay tightening monetary policy.

Furthermore, Ontario has announced a three-step plan to allow a full reopening from Covid restrictions, starting from 31 January, which should be the final green light for the central bank to hike rates 25bp. At least three more hikes are likely this year while we could also potentially hear the BoC mulling the possibility of shrinking its balance sheet later in the year.

Canada inflation (YoY%)

FX: Rate hike to support CAD, but watch for external risks

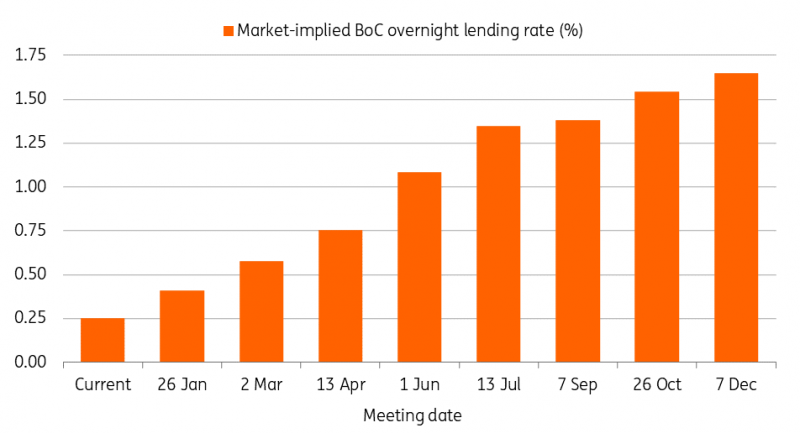

Markets are currently pricing in around a 70% implied probability that the BoC will hike rates on Wednesday. This means that there is some decent room for Canada's dollar to benefit from a rate hike, as this would also legitimise the current aggressive tightening expectations by the markets, which are pricing in around 125bp worth of hikes in 2022 (chart below).

Markets expecting five BoC hikes in 2022

We think that we could see USD/CAD move back below 1.25 on Wednesday due to the combination of a potentially USD-negative FOMC announcement (as discussed here) and the CAD-positive BoC rate hike. That said, it is not a given that the pair will be trading at current levels into Wednesday, as the fragile global risk environment – currently impacted by geopolitical tensions in Ukraine and prospects of Fed tightening – risks propping the pair higher in the short-run.

At the same time, CAD – unlike other high-beta currencies like the Australian and New Zealand dollars – can count on its positive exposure to the oil rally, with crude prices that have proven resilient in spite of adverse swings in global risk appetite.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more