Asia week ahead: Reserve Bank of Australia to decide on policy rate

Next week’s data calendar features a key policy decision from Australia, inflation numbers from Indonesia and the Philippines, plus retail sales from Singapore

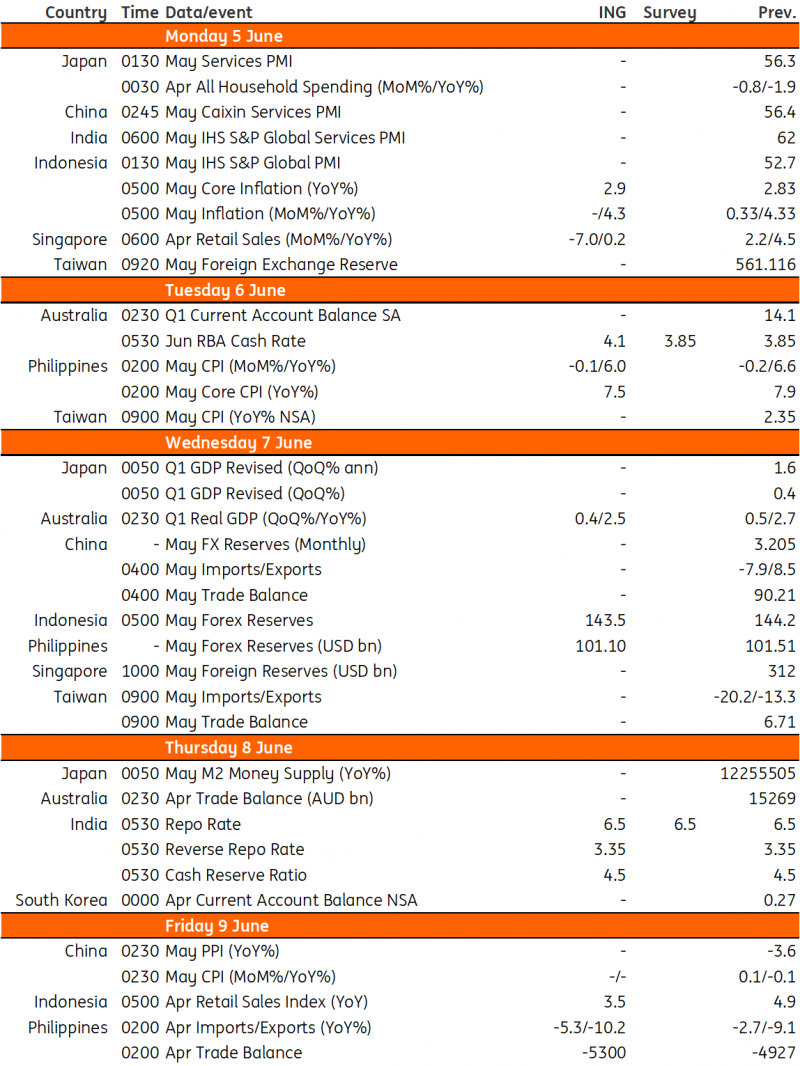

Persistent inflation could prompt RBA to hike again

The June Reserve Bank of Australia (RBA) meeting is a tough one to call. The RBA recently confused markets with its reversion to a more hawkish stance, even as inflation was weakening, and now the fall in inflation has reversed, there is a reasonable argument for it to hike again this month. However, the quarterly CPI data still seem to carry more weight than the monthly series at the moment, so some forecasters expect the RBA to wait until the August meeting when it will be able to respond to second-quarter CPI inflation.

Our forecasts are for inflation in July to have fallen to 5.2% year-on-year, but the second-quarter rate will still probably be in excess of 6%, so the RBA could well argue a further hike was needed then to ensure that inflation was falling fast enough. But with inflation rising again in April, it is going to be very hard for the RBA to sit on the sidelines in June, so a low conviction 25bp hike is our call this month, but we wouldn’t be shocked if the central bank decides to pause.

Philippine trade balance to stay in deficit on soft electronics exports

April export data is set for release next week and we could see both imports and exports remain in negative territory. Imports are expected to drop on a year-on-year basis on shrinking energy imports, while exports could face another month of contraction due to soft demand for electronics. The Philippine export sector is dominated largely by electronics, and weak global demand for smartphones and gadgets will likely impact the overall Philippine export sector. The trade gap is forecast to remain in deep shortfall ($5.1bn) which points to pressure on the Philippine peso in the near term.

Inflation readings from Indonesia and the Philippines

Headline inflation numbers for both Indonesia and the Philippines will be reported next week. We believe headline inflation will continue to cool on a year-on-year basis as favourable base effects help push the headline number back toward target. Core inflation, on the other hand, could prove to be tricky as domestic demand for both countries remains robust. Core inflation in the Philippines may inch lower to 7.5%YoY (down from 7.9%) while Indonesia may even see core inflation inch up to 2.9% from 2.8% previously. Moderating headline inflation gives both Bank Indonesia and the Bangko Sentral ng Pilipinas space to maintain policy settings, however, we don’t expect central banks to consider cutting rates just yet given the pressure on their respective currencies.

Singapore retail sales could manage to post growth

Singapore retail sales are expected to remain in expansion, although slowing from the pace reported in March. Elevated inflation is likely sapping some consumption momentum. The sustained increase in visitor arrivals however may be helping to provide retail sales a decent lift, especially for department store sales and services related to recreation. We expect retail sales to be subdued in the near term with a potential rebound should inflation decelerate towards year-end.

Key events in Asia next week

All times are Singapore time

Download

Download article2 June 2023

Our view on next week’s key events This bundle contains {bundle_entries}{/bundle_entries} articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more