Asia week ahead: China and Japan data dominate

The activity data from around the region, a lot of it from China and Japan, will be parsed for GDP growth prospects in the fourth quarter. Unfortunately, the downside risk has grown with accelerating Covid-19 infections

China data dump

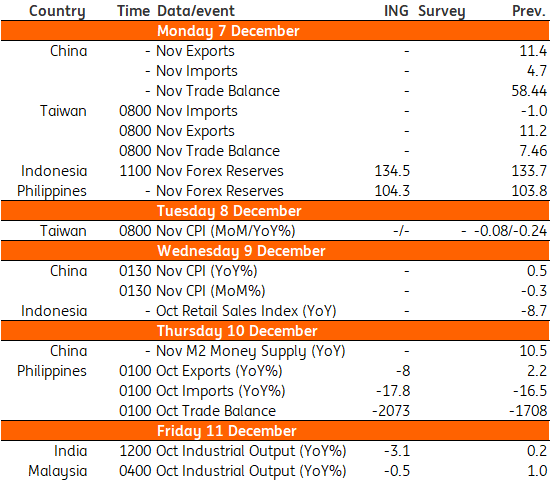

Released earlier this week, China’s Purchasing Manager Indices for November painted a rosy picture of the economy, driven by a broad-based recovery in both the manufacturing and services sectors. We will know next week whether the hard data validates this view.

The key Chinese data on the calendar are trade on Monday, followed by inflation at mid-week and monetary indicators towards the end of the week. The strong recovery in Chinese exports experienced over recent months is at risk of tapering as resurgent Covid-19 infections force some of its main trading partners into lockdown again. But domestic demand continues to recover, supporting expectations of firmer imports and new bank lending growth. All this without stoking any inflation.

Japan data dump

The Japanese releases include a revised third quarter GDP estimate. The second GDP estimate typically doesn’t differ much from the first (+5.0% QoQ in 3Q) so the markets will likely pay more attention to indicators on growth in the current quarter. There are plenty of these due next week, including October labour earnings, household spending, machinery orders and the current account.

However, the downside growth risk has probably intensified with accelerating Covid-19 caseloads, both locally and globally.

And the rest

Taiwan’s November trade figures may provide more insight into the electronics cycle. Released earlier this month, the more than 16% year-on-year surge in Korea's semiconductor exports in November bodes well here. Electronics are also a dominant part of the Philippines' exports and October figures will be out next week. Philippine exports have been the weakest in Asia this year with about a -14% YoY fall in the first nine months of the year, a trend which is likely to continue for the rest of the year. Our house forecast for October is -8%.

India and Malaysia’s industrial production releases for October come as early indicators of GDP growth of these economies in the final quarter of 2020. We see IP growth swinging back into negative territory in both, following on from renewed export weakness there.

Asia Economic Calendar

Download

Download article4 December 2020

Our view on next week’s key events This bundle contains {bundle_entries}{/bundle_entries} articles"THINK Outside" is a collection of specially commissioned content from third-party sources, such as economic think-tanks and academic institutions, that ING deems reliable and from non-research departments within ING. ING Bank N.V. ("ING") uses these sources to expand the range of opinions you can find on the THINK website. Some of these sources are not the property of or managed by ING, and therefore ING cannot always guarantee the correctness, completeness, actuality and quality of such sources, nor the availability at any given time of the data and information provided, and ING cannot accept any liability in this respect, insofar as this is permissible pursuant to the applicable laws and regulations.

This publication does not necessarily reflect the ING house view. This publication has been prepared solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved.

ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam).