A February Bank of England rate hike? It’s 50:50

The chances of a Bank of England rate hike in February are rising. Inflation is set to peak higher than previously expected, while Omicron's damage is likely to be lower and less long-lasting than past waves. We think the odds are about 50:50 for a February move, though we narrowly suspect policymakers will wait until May to fully assess the hit from Covid-19

A February rate rise is growing more likely

Will the Bank of England hike rates again at the start of February? Markets think the answer is yes. We narrowly reckon the committee will wait until May, though February’s meeting is looking much more 50:50 than it did just a few weeks ago.

Partly, that’s because it looks like Omicron’s economic damage will be neither huge nor long-lasting.

True, staff shortages are a pressing issue for most firms, while the latest card spending data shows social spending fell off a cliff in late December. There’s a decent case for waiting for more data, as the committee did last November, and that’s why we’re still leaning towards a rate hike in May. A negative December and January GDP reading look likely.

But equally last month’s rate hike decision – taken as Omicron’s wave was well underway in London – shows that the committee, like the Fed, is placing decreasing emphasis on Covid-19. In the absence of tighter restrictions, much could depend on whether cases and hospitalisations have peaked nationally much before the 3 February meeting.

Inflation is set to peak above 6%

Perhaps more importantly, inflation is clearly going to peak much higher than the Bank (and ourselves) expected only a few months ago. We’re forecasting a high of roughly 6.5% in April, and expect headline CPI to end 2022 close to 4%.

Unsurprisingly, this is heavily linked to the spike in gas and electricity prices. In fact for most of 2022, electricity alone is likely to be contributing over two percentage points to those headline inflation rates.

Contributions to UK headline inflation rates

So far, households have been insulated from the bulk of the recent cost pressure by the semi-annual price cap system. However, the next update in April – which will be calculated using average futures prices between last August and the end of this month – looks set to deliver a 50% increase in household energy prices. At their peak before Christmas, gas prices were pointing to an increase in excess of 60%.

What’s more, if futures prices were to stay where they are today (a big ‘if’, admittedly), our estimates suggest we could see something like another 15% rise this October.

The Bank of England’s Governor Andrew Bailey, along with other hawkish committee members, have previously sounded the alarm about higher headline inflation and the possible feed-through to expectations and future inflation rates. There has already been an uptick in some measures of consumer inflation expectations, though in practice these tend to track current CPI rates. We're a little less convinced that higher UK inflation rates in isolation will drive the wage/price spiral that hawkish BoE members are concerned about.

Nevertheless, with the jobs market also looking fairly tight, the Bank is set to hike rates further. And a higher inflation peak means policymakers may be more tempted to move again in February.

Households set to see a sharp rise in energy prices this year

Don't expect a rapid string of rate rises this year

But whether it’s enough to convince policymakers to hike Bank rate as far as 1% by August, as markets are now pricing, seems much less likely.

The flip side of higher electricity prices is a sharp cost of living crunch. Wage growth is hard to pin down right now owing to various data distortions. Vacancies are high, but wage pressures appear less powerful than they are in the US. It’s highly unlikely that pay will keep pace with price gains for most (if not all) of this year. That will cap consumer spending growth in coming quarters.

We also think headline inflation will fall below target in 2023, pretty much whatever happens to electricity prices next year. Admittedly energy costs could stay fairly volatile, which as we’ve written before, is partly linked to the UK’s reliance on wind, solar and gas for power (as well as very low gas storage capacity). Our commodities team also expects gas prices to stay supported for the time being.

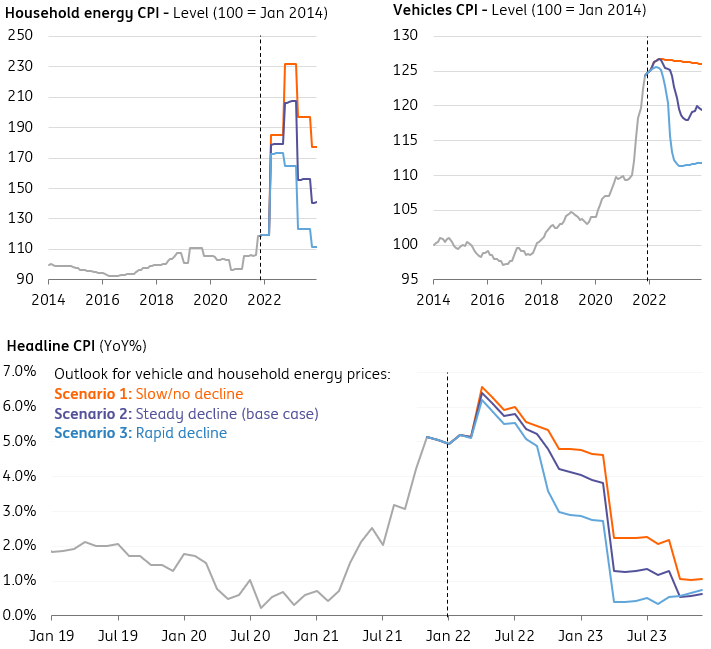

Even so, a fall in the household energy cap seems likely by April 2023, and by then we may have also seen a bit of mean-reversion in used car prices. These have risen by 30% in the past six months, but should fall back as supply chains improve through this year – though how quickly and steeply prices will correct, is much harder to pin down.

We’ve put together three illustrative scenarios for electricity and car prices in the chart below, and each show that inflation will most likely be below target by the latter parts of 2023.

UK inflation scenarios based on different paths for electricity/car prices

Does this matter for the Bank of England? You could argue not, given that neither energy nor car prices are things it can control. But it is another argument against worrying too much about higher UK inflation rates this year. And that suggests we're more likely to only get two rate rises spread across 2022, not least because the Bank also plans to begin shrinking the size of its balance sheet in tandem.

Ultimately, a lot will hinge on wages - and where the data takes us later this year once the pandemic's distortions begin to fade.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more