2022 FX Outlook: Liquid Allsorts

It's hard to pinpoint a clear central theme for FX in 2022. The Fed lift-off should help the dollar, but not across the board. Commodity currencies are still favoured, but some more than others. And some Emerging Market currencies look much better positioned than others for a year of higher interest rates. We pick out our favourites from 2022’s assorted mix

2022 stands to be a further year of convalescence and recovery in the global economy. Headwinds from the pandemic and supply chain disruption continue to blow. Yet an increasing number of policymakers are confident enough to place inflation ahead of growth concerns and embark on monetary tightening cycles.

All indicators point to strong US growth in 2022 (near 5%), persistent inflation and a Fed ready for policy rate lift-off. We expect further dollar strength against the euro and the yen through 2022, where the ECB and the BoJ have a much stronger case to keep policy loose. We see the Fed cycle as being prone to being re-priced higher and gentle dollar strength as a constant theme for 2022.

Unless backed by commodity exports, we expect European currencies, in general, to underperform against the dollar in 2022. More exposed to supply chain disruption via the greater weight of manufacturing in their economies, most will be dragged lower as EUR/USD softens through the year. Out-performing steep forward curves should be the energy exporters of NOK and RUB.

Within CEEMEA, the Czech National Bank has set the pace for tightening and is not done yet. Hungary and Poland have been a little slow out of the blocks, but light foreign positioning suggests the downside for the zloty should be limited. Elections in Hungary make the HUF a more volatile proposition. Expect the rouble to hold its gains backed by a very hawkish central bank, while the TRY and also the ZAR look more vulnerable.

In Asia, the renminbi remains an enigma. It has proven one of the strongest currencies of 2021 despite China being the epicentre of most concerns this year. Strong bond inflows and a trade surplus may have helped, yet we think the strong Renminbi has been a policy choice too. With commodity prices enjoying some mean reversion in 2022, we would expect the PBOC to allow for some trade-weighted weakening of the CNY. Within the region, we think the IDR and SGD may put up the stiffest resistance to dollar strength.

And finally, electoral poll risk will continue to stalk Latin currencies. Elections in Chile (November '21) and Brazil (October '22) pose challenges to right-wing incumbents and in Brazil’s case, fiscal risk premia could return to the BRL. Better positioned, we think, is the MXN. Banxico looks to be building a strong, precautionary wedge in local interest rates and Mexico is better positioned to enjoy US demand.

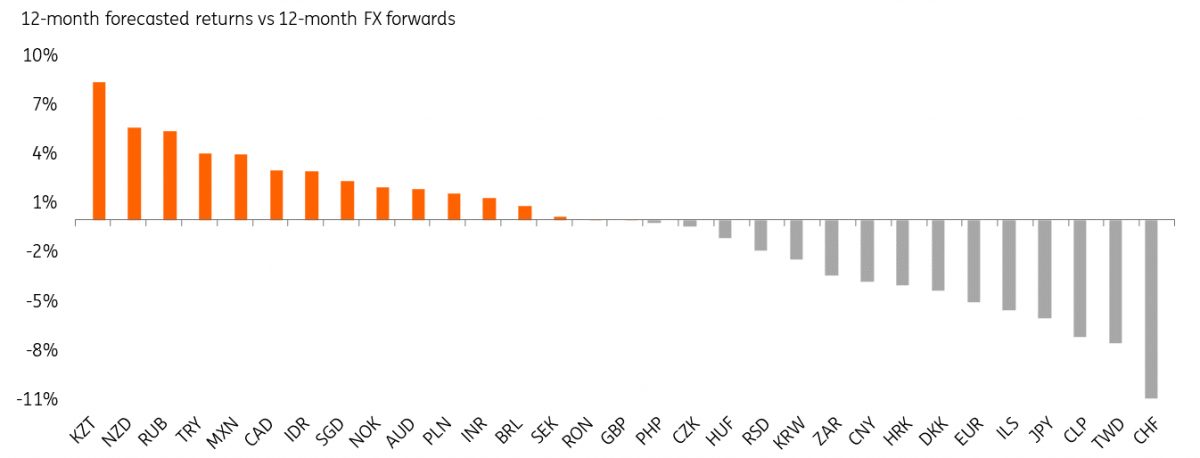

Please see below for how we think currencies can perform against their end-2022 FX forwards and see all the linked articles for more details on each of the key currency pairs.

FX forecast return versus forwards

Download

Download article

17 November 2021

2022 FX Outlook: Liquid Allsorts This bundle contains {bundle_entries}{/bundle_entries} articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more