Mexico: Recession worries deepen

GDP growth expectations have fallen everywhere in LATAM but the investment-led deceleration seen in Mexico stands out. Despite the slowdown, the government is unlikely to counter with substantial policy stimulus. Room for counter-cyclical policies is narrow, given current fiscal targets and Banxico’s effort to support the peso

It’s now three quarters with no growth

Even though the deceleration in economic activity is a global phenomenon, the sharp deceleration seen in Mexico since 4Q18 stands out. This suggests that, apart from global trade uncertainties, domestic factors are also affecting activity dynamics in a material way.

The deceleration is broad-based, affecting both industrial and service-sector indicators. But components of the domestic demand more closely associated with business sentiment, such as capital investment, has been affected the most.

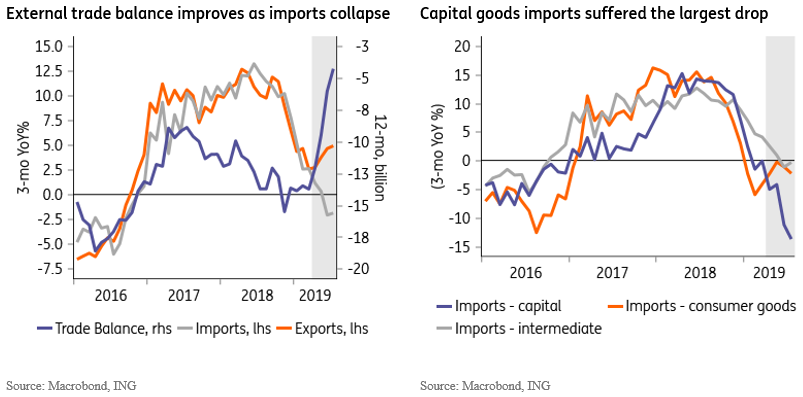

As the chart below illustrates, the ongoing decline in investment coincided with the announcement, at the end of October 2018, by Andres Manuel Lopez Obrador (AMLO), then president-elect, that he would stop the construction on the new Mexico City airport.

Data suggests that the Texcoco Airport’s termination was a turning point

Even though this was a key campaign promise, many seemed to have expected that a compromise solution would be found as the airport construction was substantially underway, and the administration would have to incur substantial costs to abandon the project.

In any case, the chart above suggests that, more than AMLO’s July 1 2018 election victory, the airport’s termination may have been a turning point that marked the effective beginning of the new administration. For many, this decision signaled that ideological stances would prevail and that room for pragmatism and compromise solutions was narrower than previously assumed.

As the charts below show, external trade data also provides additional notable evidence of domestic demand weakness, particularly investment.

The administration’s decision to freeze future rounds of oil exploration auctions and to seek arbitration remedy against gas pipeline owners, which helped trigger the resignation of Finance Minister Carlos Urzua, was seen as further evidence that businesses now operate under a changed and less certain economic environment in Mexico.

And this is not just due to AMLO’s new policies, but also due to President Trump’s repeated tariff threats, which permanently altered the outlook for Mexico’s long-standing trade relations with the US, even if the new USMCA trade agreement is eventually ratified by the three countries.

Policy reaction seen so far appears insufficient to reverse growth dynamics

AMLO’s economic program relies heavily on boosting PEMEX’s control over Mexico’s energy sector, to the detriment of the private sector. Regardless of the economic rationale for doing this, alienating the private sector when the federal government’s ability to invest is severely restricted appears to be a high-risk strategy. And widespread scepticism prevails, judging by recent rating agency decisions.

Boosting fiscal stimulus could precipitate a downgrade, which could result in financial instability if PEMEX gets a sub-investment grade rating. Therefore, the government is constrained in its ability to boost activity through fiscal policy.

But, similarly, the risk of additional credit rating downgrades will increase sharply if economic activity does not recover.

This puts policymakers in a delicate situation. Barring a change in business perception over the government’s policy inclinations, we see very limited room for the administration to reverse the ongoing decline in investment, increasing the risk of a vicious cycle of stagnation and credit rating downgrades.

Risk of harsh government spending cuts has increased

Commitment to fiscal responsibility remains intact, judging by the fiscal data seen so far this year and the targets for 2019-20, as proposed by Finance Minister Arturo Herrera. However, unless the economy turns around quickly, that commitment will be increasingly tested.

Achieving the publicly-stated fiscal targets will require stronger-than-expected spending cuts. Still, despite the low growth, AMLO appears committed to curbing spending to maintain fiscal discipline.

In the recently-released budget for next year, the government projects a sharp acceleration in GDP growth, to 2% from what we expect to be 0.3% this year. Oil production is meanwhile expected to jump by 7% on average in 2H19, relative to 1H19, and then jump 13% year-on-year next year. Such numbers would mark a remarkable turnaround by PEMEX, after several years posting large yearly reductions.

These numbers illustrate why “optimistic” is probably the most often used characteristic ascribed to the budget. Having said that, it’s hard to dispute the government’s stated commitment to a prudent fiscal stance, which suggests that expenditure will be under downside pressure, and that government consumption/investment will continue to contract.

Ultimately, however, fiscal uncertainties should linger because, if the government aims to keep its promise to not raise taxes while maintaining fiscal discipline and avoiding a rise in public debt, it will have to curb spending more aggressively than currently expected. This would prevent any effort to engineer a fiscal stimulus and, in fact, would add near-term downside to GDP growth.

Banxico guidance shows risk of under-delivering on rate cuts

AMLO has considerably less control over central bank (Banxico) policy but, by all accounts, he appears committed to upholding the bank’s autonomy. AMLO has, so far, appointed only 2 of the 5 board members, but he’ll have the opportunity to appoint a majority in the board at the end of next year, when Javier Guzmán’s term is set to expire.

Banxico launched an easing cycle in its last policy meeting, on August 15, cutting the policy rate by 25 basis points to 8.0%. That decision surprised quite a few in the market, but policy guidance remains timid in its conviction regarding future rate cuts.

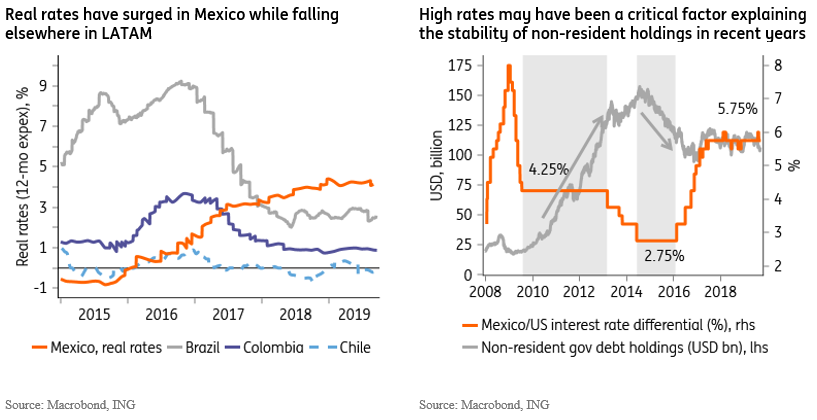

In any case, the fact that Banxico’s cut followed the US Fed’s own 25bp rate cut shows that the bank’s reaction function remains remarkably stable in recent years. As seen in the chart below, for more than 2 years now Banxico has kept the Mexico/US rate differential stable at a high 5.75%. And, we suspect, the bank should continue to follow that formula in the upcoming months.

As seen in the charts above, monetary policy is considerably tighter in Mexico when compared to other inflation-targeters in LATAM and these high rates, specifically relative to the US, has coincided with a period of fairly steady non-resident holdings in the local market.

In addition, this has also been a period during which the Mexican peso has outperformed its EM peers (see chart below). And this suggests that high local rates may have played a critical role in the stabilization of the MXN over the past couple of years, a period of heightened uncertainty north and south of the border.

In fact, Banxico’s policy strategy may be characterized as “successful” in at least this one important metric for Mexico: FX stability. As the chart above shows, the Mexican peso has been a consistent outperformer since AMLO’s election on July 1 2018. Even periods of intense sell-off in local assets, such as the aftermath of the airport cancelation in November/December 2018, faded subsequently, leaving no apparent aftereffects.

We suspect this “success” in terms of FX stability is a significant factor shielding monetary policy from political pressure.

US Fed remains a chief near-term catalyst for Banxico

The US Fed rate cut this week should once again act as an important catalyst for Banxico to cut the policy rate from 8.0% to 7.75% next week, on September 26.

But there are other reasons for the bank’s policy guidance to become, on balance, more dovish. Policymakers should acknowledge the lower-than-expected inflation, which collapsed over the past couple of months, and the slowdown in economic activity seen lately.

Still, we expect the dovish shift to continue to be moderated by policymakers’ caution with some elements of recent inflation trends, and the elevated policy uncertainty. Regarding inflation, headline inflation has fallen sharply, and is now very close to the target at 3.2% YoY. But this contrasts with the higher prints still prevailing for the CPI’s core component, now at 3.8%, and the still un-anchored inflation expectations.

Moreover, as we’ve discussed before, Banxico could have considerable room to ease policy conditions beyond any move implemented by the US Fed. However, persistent risks of financial market instability triggered by PEMEX/fiscal concerns, or renewed US-Mexico trade-related tension, suggest that bank officials should proceed cautiously.

The neutral level for the nominal policy rate is likely close to 6%, down from 8% now, but FX considerations will remain crucial in Banxico’s reaction function. In practice, high rates should continue to act as the chief FX anchor and policymakers should aim to maintain a large interest-rate differential between Mexico and the US, to prevent outflows.

Our expectation is for Banxico to continue to follow the US Fed’s lead in the very near term. Assuming a total of 100bp in cuts by the US Fed during this mid-cycle adjustment, with one additional cut in 4Q and another in 1Q20, Banxico should bring the overnight rate to 7.25% by 1Q20.

Beyond that, much should depend on the FX trajectory and Banxico’s confidence in the fiscal policy trajectory being implemented by the Finance Ministry. The bias is decidedly in favour of additional cuts, with a moderate and less frontloaded cycle towards 6.50-6.75% over the next couple of years probably seen as an appropriate trajectory. But our level of conviction is quite low at this stage.

This compares with the curve pricing a frontloaded cycle with close to 150bp in additional cuts, to 6.5%, by mid-2020. Analyst surveys show, meanwhile, a considerably shorter cycle, with just one 25bp additional cut this year and 75bp in cuts next year, to 7.0%.

For the Mexican peso, our expectation is that high interest rates should remain an effective stabilizing factor, which should keep the USDMXN trading near-equilibrium, close to 19.5 in the coming quarters.

"THINK Outside" is a collection of specially commissioned content from third-party sources, such as economic think-tanks and academic institutions, that ING deems reliable and from non-research departments within ING. ING Bank N.V. ("ING") uses these sources to expand the range of opinions you can find on the THINK website. Some of these sources are not the property of or managed by ING, and therefore ING cannot always guarantee the correctness, completeness, actuality and quality of such sources, nor the availability at any given time of the data and information provided, and ING cannot accept any liability in this respect, insofar as this is permissible pursuant to the applicable laws and regulations.

This publication does not necessarily reflect the ING house view. This publication has been prepared solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved.

ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam).